NO.PZ2020021204000018

问题如下:

A three-year bond with a face value of USD 100 pays coupons annually at the rate of 10% per year. Its yield is 7% with annual compounding. What are (a) the Macaulay duration, (b) the convexity, (c) the modified duration, and (d) the modified convexity?

解释:

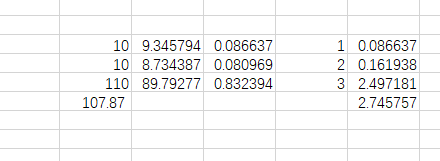

The Macaulay duration is 2.7458, the convexity is 7.9021,

and the modified duration is

2.7458 / 1.07 = 2.5661

The modified convexity is

7.9021/1.072 = 6.9020

自认为与讲义公布公式一致,但是答案计算多次不对,找不到原因。