NO.PZ2019070901000091

问题如下:

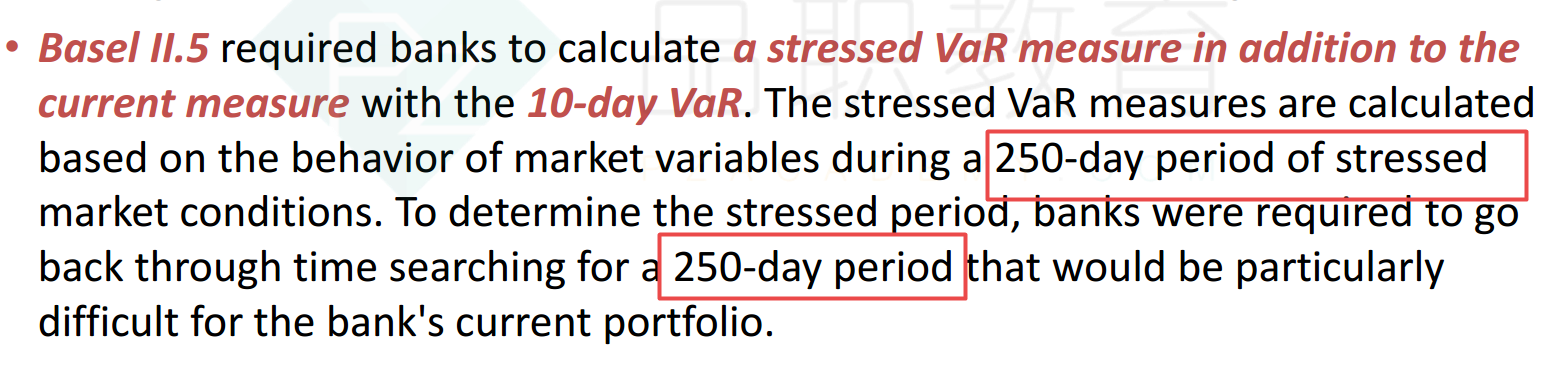

Basel II.5 added stressed VaR calculation in market risk measurement, Which of the following statements about stressed VaR is not correct?

选项:

A.Banks should identify a one-year priod as the "stressed period", the period may be different across banks.

B.Due to the stressed VaR, the market risk capital charge under Basel II.5 should be at least twice the market risk capital charge under Basel II.

C.For the purpose of prudential calculating market risk capital charge, the stressed VaR replaces the normal VaR.

D.The stressed VaR calculation uses a 99% confidence level, 250-day period of stressed market conditions.

解释:

C is correct.

考点:stressed VaR

解析:巴塞尔协议II.5要求银行计算两个VaR,normal和stressed。总市场风险资本是normal VaR和stressed VaR的总和.

最初,监管机构认为2008年是“stressed period”的理想选择。 银行现在需要确定其投资组合表现最差的一年,所以有些银行可能还有表现比2008年更差的年份可以作为stressed VaR的数据来源。A对。

stressed VaR一般比normal的大,总市场风险资本是他俩的加和,所以比起之前单算normal var的情况,市场风险资本最少也要翻倍。B对。

stressed VaR是在normal VaR的基础上增加的部分,并没有replace normal VaR。C错。

D描述的是正确的stressed var的估计方法,正确。

d为什么不是99% 10days