NO.PZ2016082404000026

问题如下:

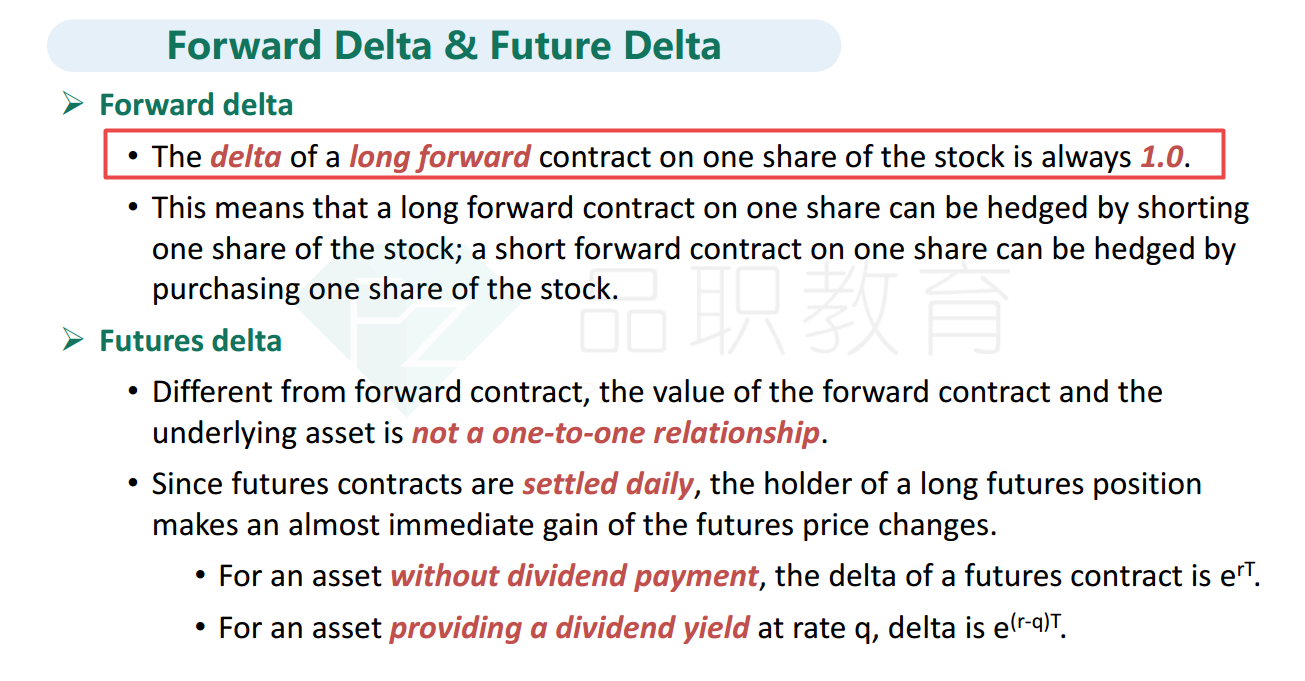

The dividend yield of an asset is 10% per annum. What is the delta of a long forward contract on the asset with six months to maturity?

选项: A. 0.95

B.

1.00

C.

1.05

D.

Cannot determine without additional information

解释:

ANSWER: A

The delta of a long forward contract is

这是哪的知识点???