NO.PZ2020011303000087

问题如下:

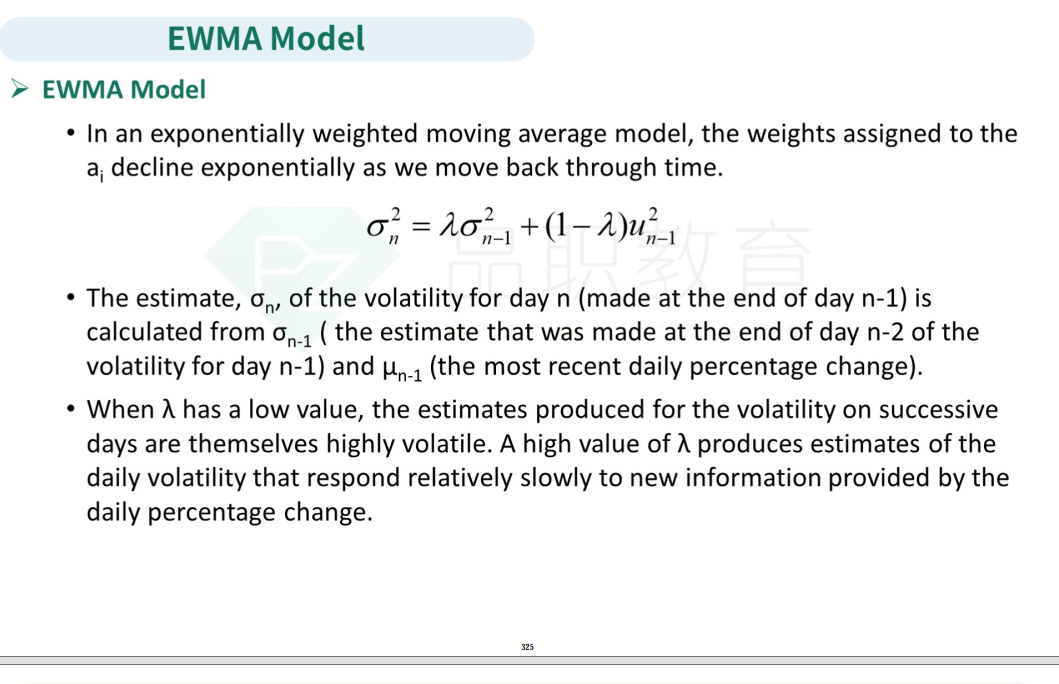

Suppose that the price of asset X at the close of trading yesterday was USD 40 and its volatility

解释:

The new estimates of the variance rate of X is

0.95 × 0.015^2 + 0.05 × (−2/40)^2 = 0.000339

which corresponds to a new volatility of 1.84%. The new volatility for Y is1.67%. The

0.95 × 0.000102 + 0.05 × (−2/40) × (0.1/10) = 0.0000719

The new correlation is 0.0000719/(0.0184 × 0.0167) = 0.23.

题目问:已知X资产昨日的收盘价是40,日波动率是1.5%。Y资产的昨日收盘价是10,日波动率是1.7%,X和Y今日收盘价是38和10.1,相关系数是0.4,λ是0.95,通过EMWA模型来计算一下新的X和Y的波动率以及correlation。

Xvolatility=[0.95 × 0.015^2 +0.05 × (−2/40)^2]^0.5=1.84%

Y volatility=1.76%

covariance=0.95 × 0.000102+ 0.05 × (−2/40) × (0.1/10) = 0.0000719

The new correlation is 0.0000719/(0.0184 × 0.0167) =0.23

可以讲一下变化之后的X,Y的volatility怎么算吗,老师讲过这个公式吗