NO.PZ2020021601000002

问题如下:

Viktoria Smith is a recently hired junior analyst at Aries Investments. Smith and her supervisor, Ingrid Johansson, meet to discuss some of the firm’s investments in banks and insurance companies.

Smith and Johansson discuss key aspects of financial regulations, particularly the framework of Basel III. Johansson tells Smith:

"Basel III specifies the minimum percentage of its risk-weighted assets that a bank must fund with equity. This requirement of Basel III prevents a bank from assuming so much financial leverage that it is unable to withstand loan losses or asset write-downs."

The aspect of the Basel III framework that Johansson describes to Smith relates to minimum:

选项:

A.

capital requirements.

B.liquidity requirements.

C.amounts of stable funding requirements.

解释:

A is correct.

Basel III specifies the minimum percentage of its risk-weighted assets that a bank must fund with equity capital. This minimum funding requirement prevents a bank from assuming so much financial leverage that it is unable to withstand loan losses or asset write-downs.

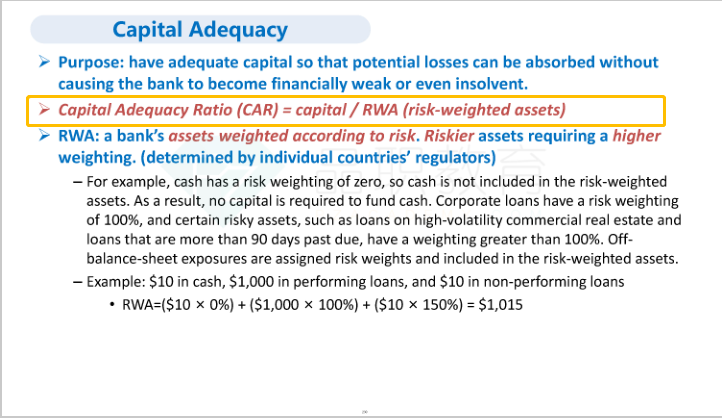

解析:巴塞尔协议三明确了银行的资本必须达到风险加权资产的最小比例。指的是资本充足率:capital adequacy ratio(CAR)=capital/RWA(risk-weighted assets)。

老师您好,请问下在课件哪里有提到CAR的公式?