NO.PZ2018113001000073

问题如下:

Darnell, a portfolio manager, makes two

statements about the implied volatility.

Statement 1: The volatility smile shows

that OTM puts have higher implied volatility than ATM puts

Statement 2: The volatility skew shows that

the ITM put has higher implied volatility compared to the ATM put.

Which of the following statements is true?

选项:

A.Statement 1

Statement 2

Both

解释:

A is correct

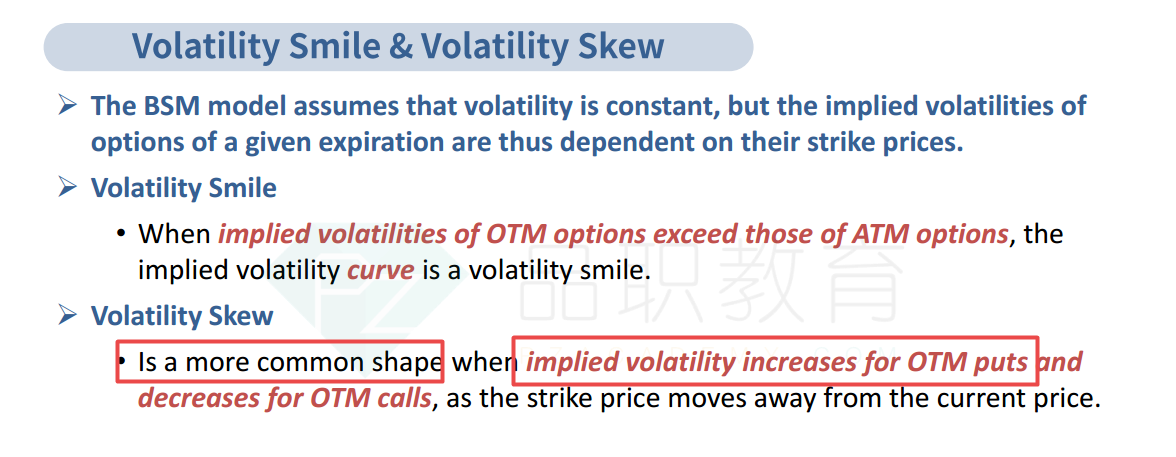

由下图可知:volatility smile显示OTM或者ITM的看跌期权对应的隐含波动率,都高于ATM状态下的看跌期权的隐含波动率,因此表述1正确。

volatility skew显示,OTM的看跌期权对应的隐含波动率高于ATM状态下的看跌期权隐含的波动率;而ITM的看跌期权的隐含波动率低于ATM的看跌期权的隐含波动率。

在volatility smile发现OTM对比ITM的put, OTM会更高一些, 这是一个正常的结论吗? 因为老师上课画的volatility smile左右两边一样高, 但是原版书图形是OTM对比ITM更高一些, 那我可以总结说OTM put 比ITM put 隐含波动性更高吗?