NO.PZ2016031001000079

问题如下:

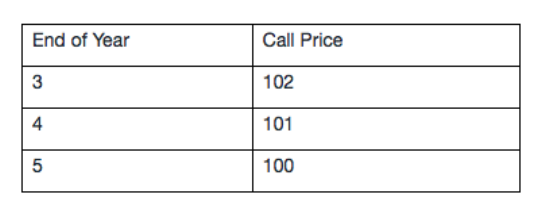

A bond with 5 years remaining until maturity is currently trading for 101 per 100 of par value. The bond offers a 6% coupon rate with interest paid semiannually. The bond is first callable in 3 years, and is callable after that date on coupon dates according to the following schedule:

The bond’s annual yield-to-second-call is closest to:

选项:

A.

2.97%.

B.

5.72%.

C.

5.94%.

解释:

C is correct.

The yield-to-second-call is 5.94%. Given the second call date is exactly four years away, the formula for calculating this bond’s yield-to-second-call is:

where:

PV = present value, or the price of the bond

PMT = coupon payment per period

FV = call price paid at call date

r = market discount rate, or required rate of return per period

r = 0.0297

To arrive at the annualized yield-to-second-call, the semiannual rate of 2.97% must be multiplied by two. Therefore, the yield-to-second-call is equal to 2.97% × 2 = 5.94%.

考点:YTC

解析:求的是yield-to-second call,第二次赎回价格为101,因此FV=101,N=4×2=8,PMT=3,PV= -101,求得I/Y=2.97,再乘2得YTC为5.94%,故选项C正确。

按计算器的时候,N=8,PMT=3,FV=101,PV是怎么算出来的呀