NO.PZ2020021205000066

问题如下:

what position should be taken in the two options and the underlying asset for delta, vega, and gamma neutrality?

解释:

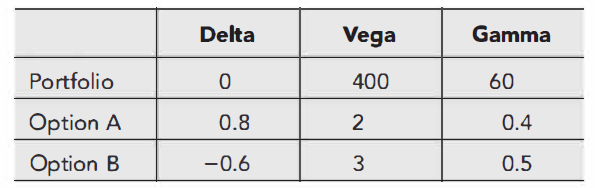

If the position is Xa in option A and Xb in option B we require

400 + 2Xa + 3Xb =0

60+0.4Xa + 0.5Xb=0

The solution to these equations is Xa = 100, Xb = -200. The position taken should therefore be a long position of 100 in option A and a short position of 200 in option B. This creates a delta of: 0.8 X 100 + (-0.6) X (-200) = 200 It is therefore necessary to sell 200 of the asset to maintain a delta of zero.

这个公式是从哪来的?题目不知道是要求算什么东西,达到什么样的目的?谢谢