NO.PZ2018062010000023

问题如下:

Which bond offers the lowest yield-to-maturity?

选项:

A.

Bond A

B.

Bond B

C.

Bond C

解释:

A is correct.

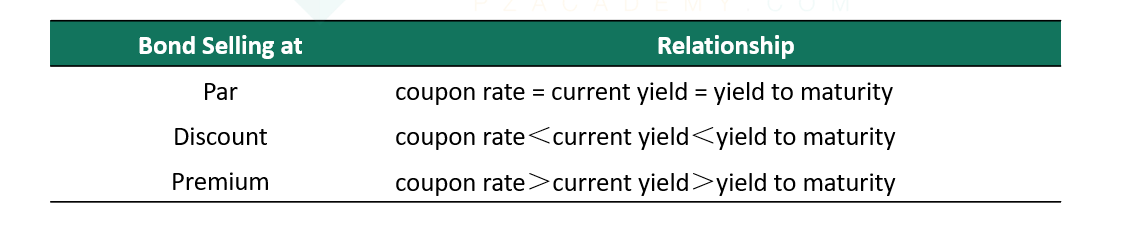

Bond A's price > par, so A's YTM is lower than its coupon rate, which is 7%.

Bond B's price = par, so B's YTM is equal to its coupon rate, which is 8%.

Bond C's price < par, so C's YTM is higher than its coupon rate, which is 7%.

So bond A offers the lowest YTM.

考点:YTM

解析:债券A价格大于面值,所以债券A的YTM低于其coupon rate (7%);债券B的价格等于面值,所以债券B的YTM等于其coupon rate (8%);债券C的价格小于面值,所以债券C的YTM高于其coupon rate (7%)。所以债券A的YTM最低,故选项A正确。

为什么价格大于面值,ytm就要大于coupon rate呢?在哪里有讲到