NO.PZ2020010304000045

问题如下:

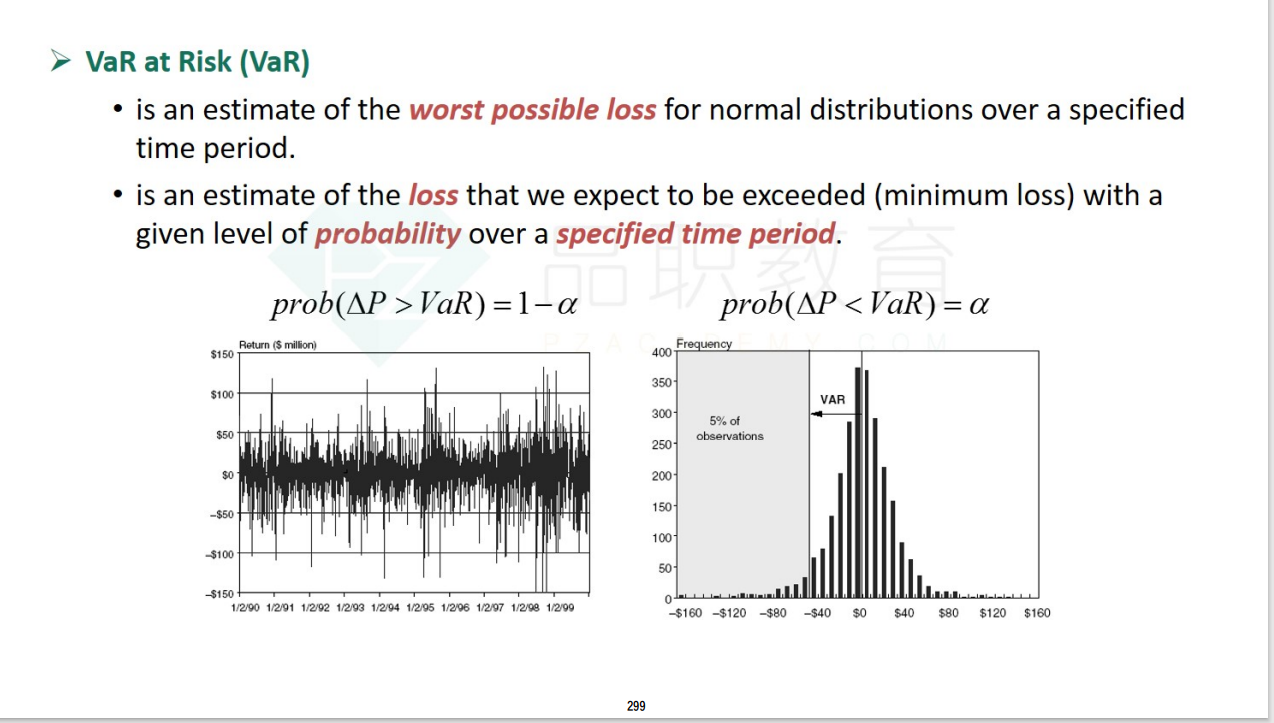

What does the VaR of a portfolio measure?

选项:

解释:

The VaR is a measure or the magnitude of the loss that the portfolio will lose with some specified probability (e.g., 5%) over some fixed horizon (e.g., one day or one week). The p-VaR is formally defined as the value where:

Pr(L > VaR) = 1 - p,

where L is the loss of the portfolio of the selected time horizon and 1 - p is the probability that a large loss occurs.

老师不好意思,想问一下这是哪个考点?