NO.PZ2015121801000068

问题如下:

An analyst has made the following return projections for each of three possible outcomes with an equal likelihood of occurrence:

If the analyst constructs two-asset portfolios that are equally weighted, which pair of assets provides the least amount of risk reduction?

选项:

A.

Asset 1 and Asset 2.

B.

Asset 1 and Asset 3.

C.

Asset 2 and Asset 3.

解释:

A is correct.

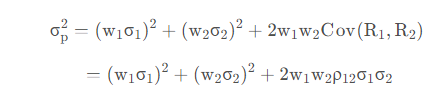

An equally weighted portfolio of Asset 1 and Asset 2 has the highest level of volatility of the three pairs. All three pairs have the same expected return; however, the portfolio of Asset 1 and Asset 2 provides the least amount of risk reduction.

这题已经算出了相关系数0.5,-0.5,-1。但是在比较的时候,以往认知是说绝对值越大,相关性越大,相关系数等于0,相关性最小。不太理解为什么这题不看绝对值呢。