NO.PZ2020021203000078

问题如下:

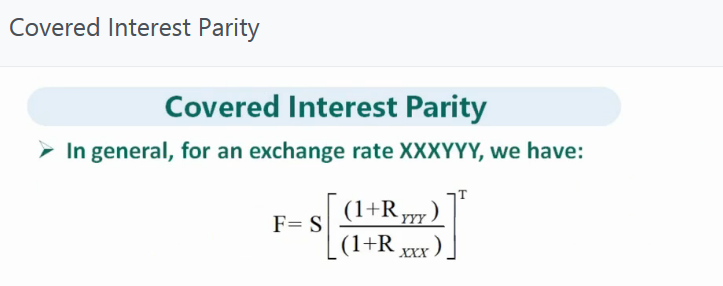

Use the results in Chapter 9 to determine put-call parity for a currency options on the GBP/USD exchange rate. Express your answer in terms of the USD risk-free rate, RUSD, the GBP risk-free rate, RGBP, and the time to maturity, T.

选项:

解释:

with equation

Substituting this into Equation Price + PV(K) = European Put Price + PV(F) and noting that:

European Call Price + = European Put Price +

这部分内容对应基础讲义哪部分?谢谢