NO.PZ2021101401000020

问题如下:

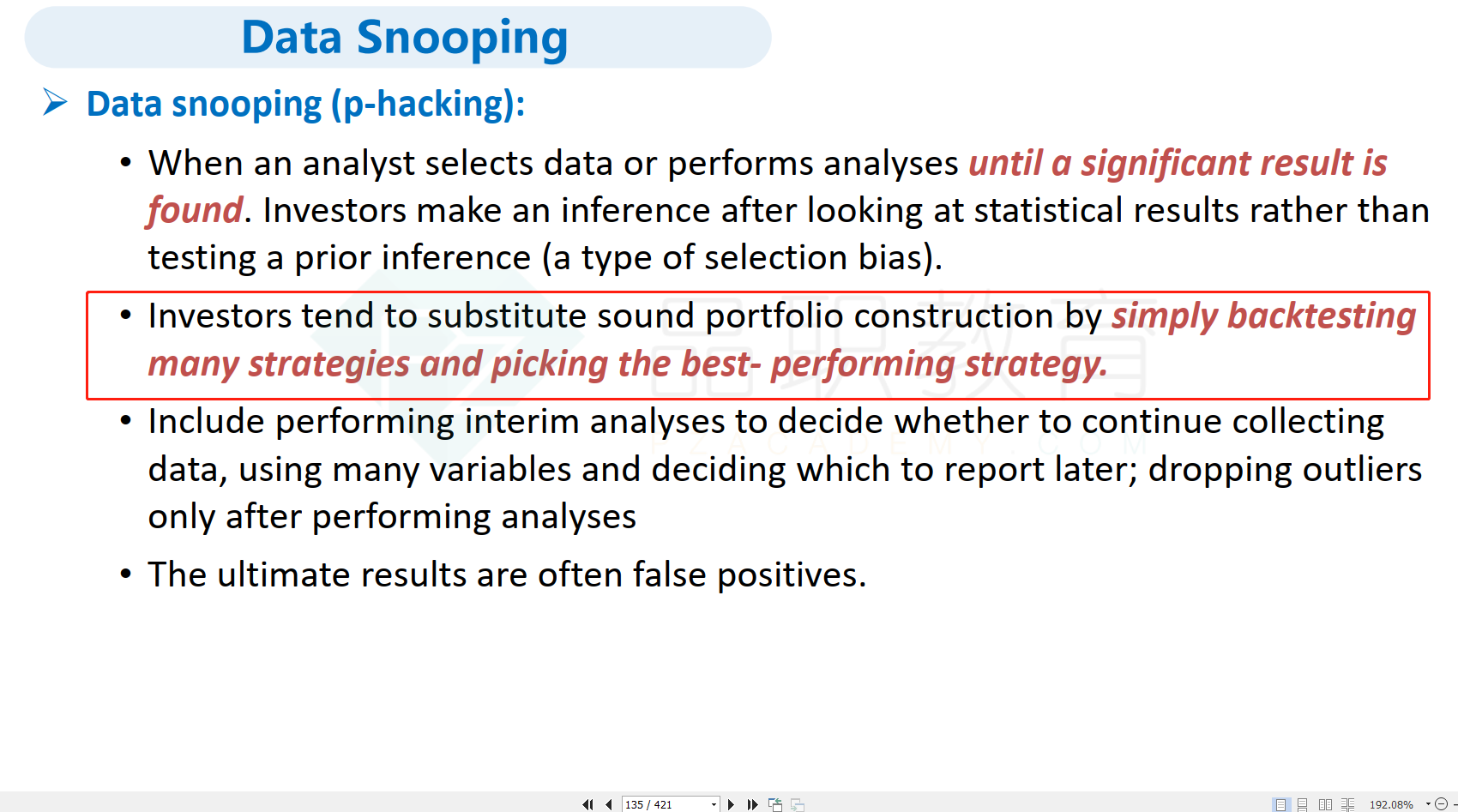

Galic is surprised to see that some of the backtest results are unfavorable. He asks, “Why has GWP not considered strategies that perform better in backtesting?” Galic recently met with Fastlane Wealth Managers, who showed much better performance results. The portfolio manager at Fastlane told Galic that the company selects the top-performing strategies after performing thousands of backtests.

The approach used by Fastlane Wealth Managers most likely incorporates:

选项:

A.

risk parity.

B.

data snooping.

C.

cross-validation.

解释:

B is correct. The fact that the two firms’ investment performance results differ over similar time horizons using the same data and factors may be the result of selection bias. Data snooping is a type of selection bias. Fastlane Wealth Managers is most likely selecting the best-performing modeling approach and publishing its results (i.e., data snooping).

A is incorrect because risk parity is a portfolio construction technique that accounts for the volatility of each factor and the correlations of returns among all factors to be combined in the portfolio. It is not regarded as selection bias.

C is incorrect because cross-validation is a technique used in the machine learning field, as well as in backtesting investment strategies, to partition data for model training and testing. It is not considered selection bias.

题干同时提到F公司管理的组合表现好,容易让人误以为题目想考的是他们通过cross validation的方式规避了data snooping