NO.PZ202207040100000305

问题如下:

Grasmere Asset Management Case Scenario

Morgan Abernathy, Nathaniel Granville, and Gabriella Carlucci are analysts at Grasmere Asset Management (Grasmere), an investment firm that offers a diversified mix of actively managed equity and fixed-income investment funds. The firm follows the fundamental approach, using both bottom-up and top-down investment management strategies. The analysts meet regularly to discuss investment ideas and related topics.

The meeting begins with a discussion of the fundamental approach to active equity management strategies. The analysts make the following statements:

The approach is a subjective investment process that uses discretion in making decisions.

The portfolio manager’s selections are based on determining a security’s exposure to selected variables that predict its return.

The construction of a portfolio is generally done using a portfolio optimizer, which controls risk at the portfolio level.

The analysts then review Exhibit 1, which describes a selection of the Grasmere equity funds.

Exhibit 1

Grasmere Equity Funds

The analysts made the following points about the potential investments that Fund B might undertake. The fund should be interested in

investing in the shares of a potential acquirer, even in a consolidating industry;

taking a control position in a distressed company’s shares selling at a deep discount to its intrinsic value; and

using its expertise to make long-term investments involving companies in reorganization.

Grasmere’s larger funds have had an impressive long-term record compared with peers. In more recent times, however, the results have been lagging. Positions have become more concentrated than in the past, and the proportion of positions underperforming their respective industries has increased. Carlucci believes managers may have become subject to two biases: an illusion of control and confirmation bias. Carlucci asks Abernathy what steps he could recommend to address the effect of these biases.

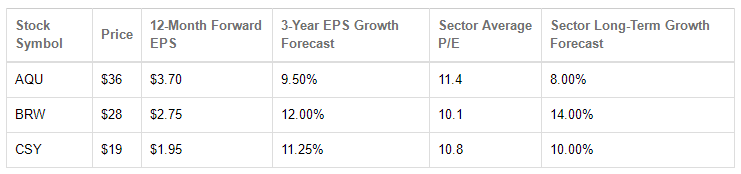

The final topic involves a discussion of some high-profile companies that recently released their full-year earnings results. Exhibit 2 contains market data and financial projections on three of the stocks discussed by Grasmere’s analysts. They are considering adding one of these stocks to Fund D.

Exhibit 2

Market Data and Financial Projections of Selected Stocks

Question

Using Exhibits 1 and 2, the stock that would be the best addition to Fund D is:

选项:

A.AQU. B.BRW. C.CSY.解释:

SolutionC is correct. Fund D follows the GARP (growth at a reasonable price) strategy, which seeks out companies with above-average growth that trade at reasonable valuation multiples. Many investors who use GARP rely on the P/E-to-growth (PEG) ratio.

AQU’s forward P/E is 36 ÷ 3.70 = 9.73, and its PEG ratio is 9.73 ÷ 9.50 = 1.02.

BRW’s forward P/E is 28 ÷ 2.75 = 10.18, and its PEG is 10.18 ÷ 12.0 = 0.85.

CSY’s forward P/E is 19 ÷ 1.95 = 9.74, and its PEG is 9.74 ÷ 11.25 = 0.87.

Although lower PEG ratios are preferred and BRW has a slightly lower PEG ratio than CSY, BRW’s EPS growth forecast of 12.00% is below the sector long-term growth forecast of 14.00% whereas CSY’s EPS growth forecast of 11.25% is above the sector long-term growth forecast of 10.00%. Given CSY’s combination of above-average growth and a reasonable valuation multiple, it would be the best addition to Fund D.

A is incorrect. AQU has the highest PEG ratio; lower PEG ratios are preferred.

B is incorrect. Although BRW has a slightly lower PEG ratio than CSY, BRW’s EPS growth forecast of 12.00% is below the sector long-term growth forecast of 14.00% whereas CSY’s EPS growth forecast of 11.25% is above the sector long-term growth forecast of 10.00%.

为什么计算PEG的时候,G去除了%来计算?