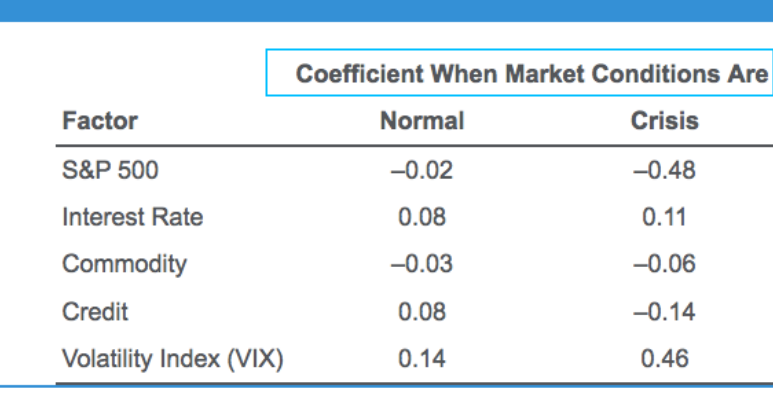

First Ocean’s fund-of-funds offering, Diversified Alpha Plus, is invested in 12 different hedge fund strategies. The factor sensitivities for Fund A during normal conditions and crisis conditions are highlighted in Exhibit 1. All exposures are significant at the 5% level.

Chang is discussing Fund A with First Ocean’s Investment Committee and makes the following observations about its role in the portfolio:

Observation 1Fund A has a dedicated short bias, which helps offset beta exposure from the long–short managers in the fund.

Observation 2The sensitivity to volatility is indicative of selling puts against some of its short positions.

Observation 3The manager has demonstrated the ability to hold long positions in deep out-of-the-money puts during periods of market stress.