可以解釋下列敘述是什麼意思嗎?是在講義的哪個地方?

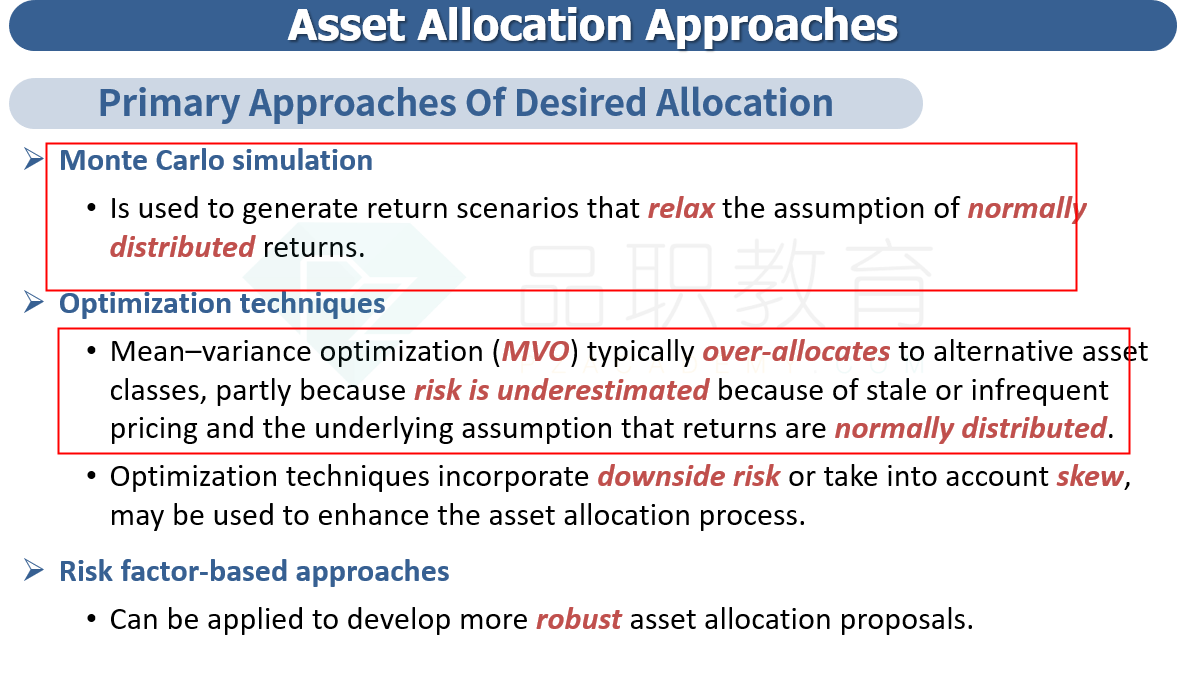

It is common for portfolio optimization that includes alternative assets to be performed in two stages—the first following a traditional mean–variance analysis and the second using Monte Carlo simulation or other more advanced techniques to account for the non-normality of returns of alternatives.

題目摘要如下:

Gill also reminds Chan, “We have used a traditional mean–variance approach to optimize your current portfolio allocation, but this will not be appropriate for a portfolio that includes substantial allocations to alternative investments. Returns to traditional asset classes are normally distributed, whereas returns to alternative investments tend to exhibit non-normality. For alternative investments, even the most basic estimate of risk, the standard deviation of returns, is likely to be measured incorrectly, because of the way returns are calculated and reported. A common approach to portfolio optimization when alternative assets are involved is a two-step process that first uses a mean–variance analysis for the traditional asset classes and then incorporates alternative assets using more sophisticated techniques, such as Monte Carlo simulation.”

Q:In his comments on portfolio optimization, Gill is least likely correct regarding the:

A. normality of asset class returns.

B. accuracy of risk estimates for alternative investments.

C. common way portfolio optimization can incorporate alternative investments.

A is correct. Despite its limitation, the assumption of normality is assumed for both traditional and alternative asset classes. The returns to traditional assets classes are not normally distributed; however, mean–variance techniques assuming normality have persisted because no standard approach for working with non-normally distributed returns exists. Many alternative asset classes exhibit more substantial skewness and kurtosis than traditional assets, partly because of high leverage, sensitivity to liquidity events, and asymmetric performance fees, making the assumption of normality more problematic, but these concerns also exist for some traditional assets (e.g., speculative grade bonds, microcap equities).

B is incorrect. Returns to alternative investments are often based on appraisal data rather than market transactions, which results in artificial smoothing and underestimation of the standard deviation of returns. Infrequent reporting also makes accurate measurement of standard deviation difficult because of limited observations.

C is incorrect. It is common for portfolio optimization that includes alternative assets to be performed in two stages—the first following a traditional mean–variance analysis and the second using Monte Carlo simulation or other more advanced techniques to account for the non-normality of returns of alternatives.