NO.PZ201803130100000101

问题如下:

The asset allocation in Exhibit 1 most likely resulted from a mean–variance optimization using:

选项:

A.historical data.

B.reverse optimization.

C.Black–Litterman inputs.

解释:

A is correct.

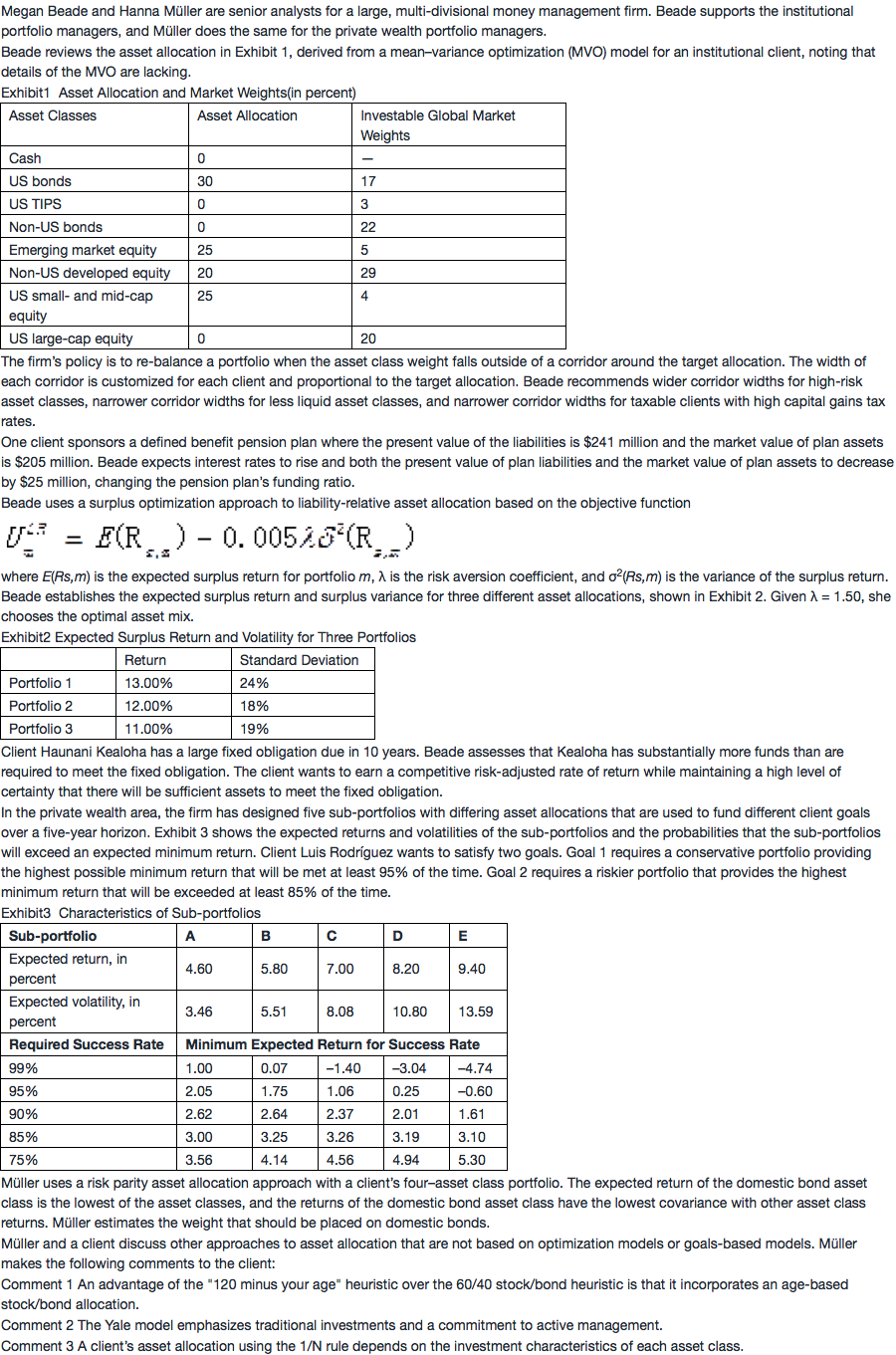

The allocations in Exhibit 1 are most likely from an MVO model using historical data inputs. MVO tends to result in asset allocations that are concentrated in a subset of the available asset classes. The allocations in Exhibit 1 have heavy concentrations in four of the asset classes and no investment in the other four asset classes, and the weights differ greatly from global market weights. Compared to the use of historical inputs, the Black–Litterman and reverse-optimization models most likely would be less concentrated in a few asset classes and less distant from the global weights.

- investable global market weights和asset allocation的权重差别非常大,因此我认为是由于加入了基金经理自己的大量观点,作为inputs,才导致这个权重。

- 我觉得是不是AA中,单一资产权重占比很高,才可以算过分集中?