NO.PZ2019052801000058

问题如下:

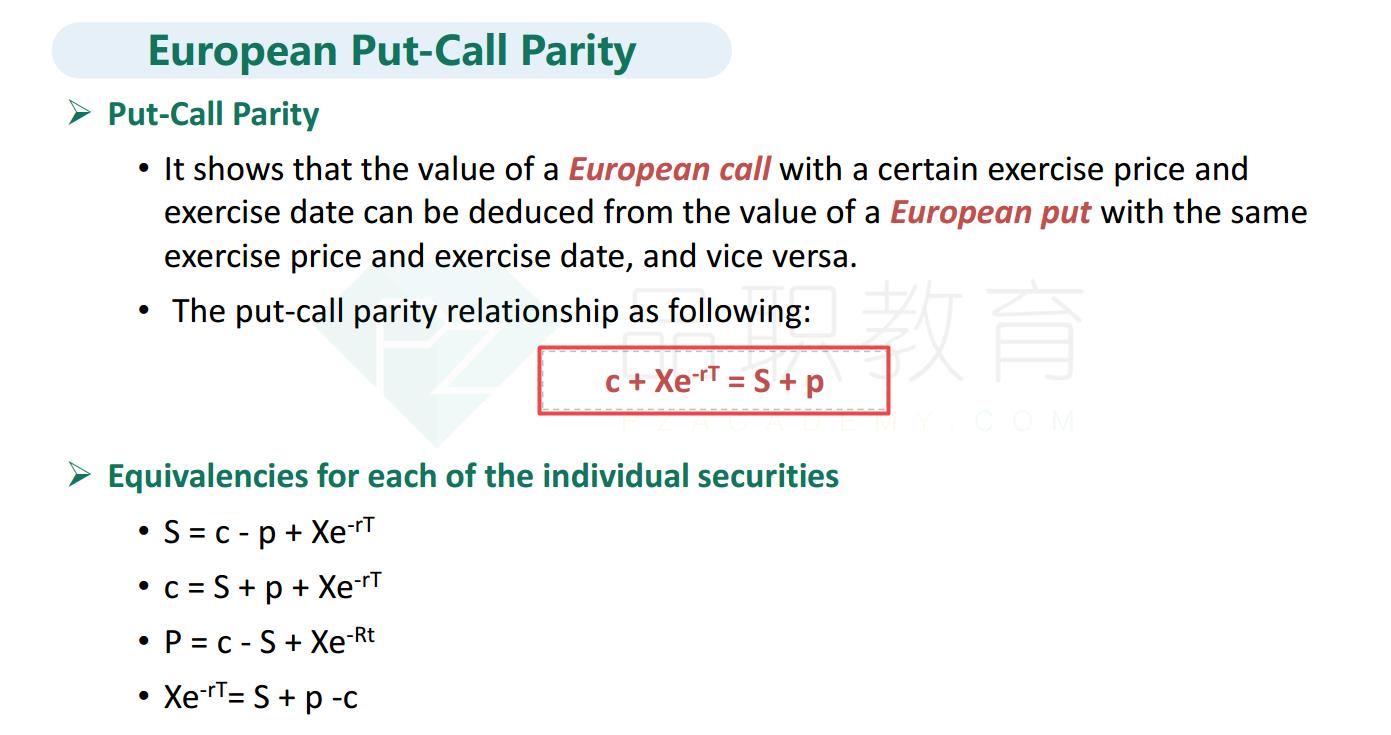

The current price of a stock is $25, an european put option on the stock has a strike price of $27 and an expiration of 9 months is priced $3, the risk-free rate is 4%,the value of the corresponding call option is close to?

选项:

A.$0.3.

B.$2.1.

C.$1.8.

D.$2.

解释:

C is correct.

考点: Put-Call Parity.

如何看出是连续复利用e做?