NO.PZ2022051904000007

问题如下:

Clive Staples is a consultant with the Leedsford Organization (Leedsford), a boutique investment consulting firm serving large endowments and private foundations. Leedsford consults on tactical asset allocation (TAA) program development, implementation, and ongoing TAA idea generation.

Staples has just completed his quarterly client review of the Narnea Foundation. Based on the Foundation’s current asset allocation and Leedsford’s updated fair value models, Staples believes there is an exploitable TAA opportunity in US large-cap growth stocks. He recommends a 2% overweight position to the US equities policy allocation either through an unlevered ETF or total return swap exposures to the Russell 1000 Growth Index.

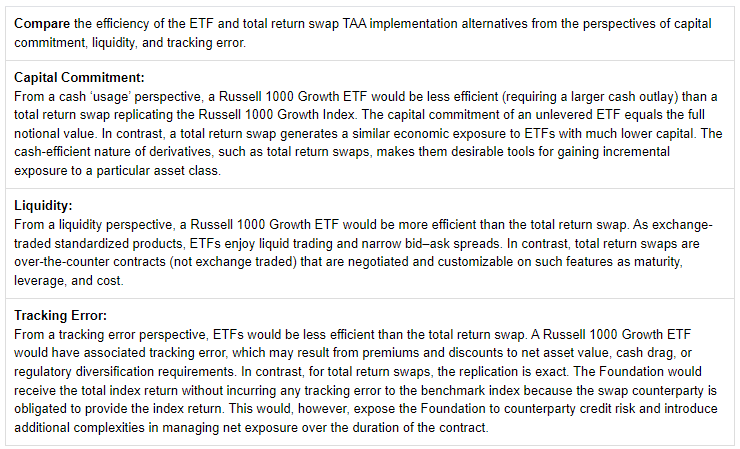

Q. Compare the efficiency of the ETF and total return swap TAA implementation alternatives from the perspectives of capital commitment, liquidity, and tracking error.

选项:

解释:

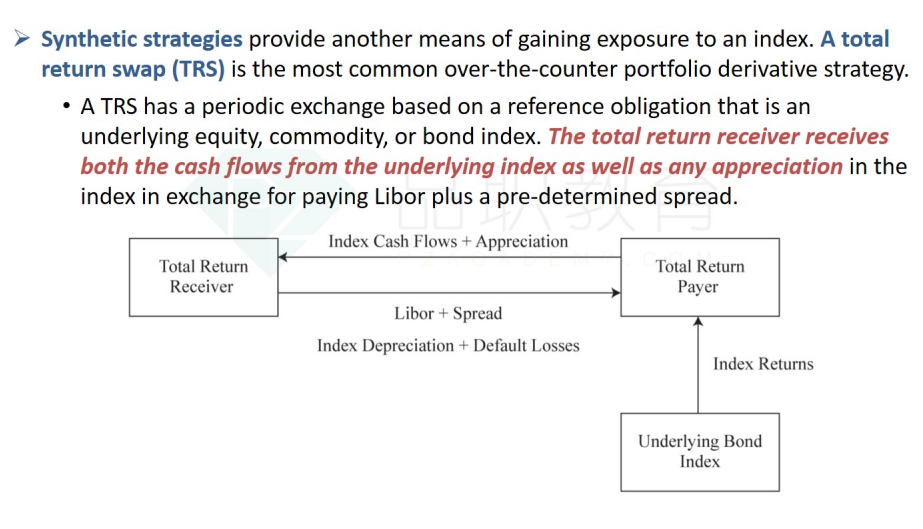

老师,total return swap为总收益的互换,想确认下以下理解是否准确:reciever收到的相当于1+R(index),而payer收到的相当于交割时的市场利率(如Libor)+spread?

此外有点忘记,这部分中的spread代表什么?是合约双方约定的一个spread吗?还是指数相对于无风险利率的spread?