NO.PZ201812100100000806

问题如下:

Based on Exhibit 3, Topmaker’s impairment loss under IFRS is:

选项:

A.$120 million. B.$300 million. C.$400 million.解释:

B is correct.

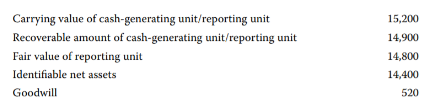

The goodwill impairment loss under IFRS is $300 million, calculated as the difference between the recoverable amount of a cash-generating

unit and the carrying value of the cash-generating unit. Topmaker’s recoverable amount of the cash-generating unit is $14,900 million, which is less than the

carrying value of the cash-generating unit of $15,200 million. This results in an

impairment loss of $300 million ($14,900 – $15,200).

考点:IFRS下goodwill减值。

解析:IFRS下的goodwill减值比较的是cash generating unit的carrying value和recoverable amount,如果carrying value高于recoverable amount,说明账面价值计的高了,需要减值,减值金额直接是二者差额=$14,900 – $15,200=$300 million。

假如这里是GAAP下呢?是不是14900-14800=100?我目前做题没发现GAAP下的情况,是因为这个考点不考吗?