请问老师,本题答案中为什么the return on bond 会增加呢???和股票有什么关系呢?

不太明白,求解答,谢谢!!!

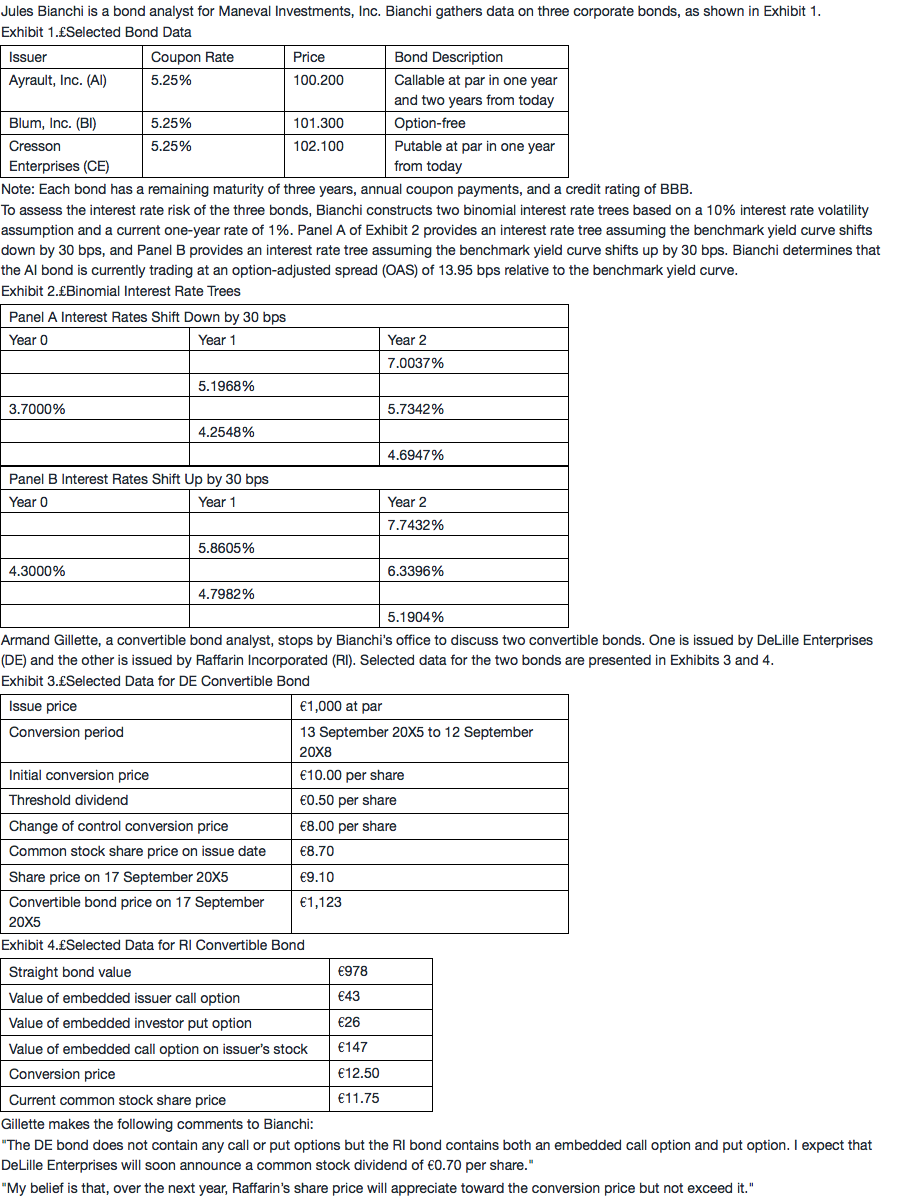

问题如下图:

选项:

A.

B.

C.

解释:

发亮_品职助教 · 2018年04月21日

同学你好。

本题Convertible bond的收益增加,来自Call option on stock的价值增加,当标的股票价格增加时,这个Call option价值增加,使得持有convertible bond的收益增加。

由于Convertible bond含有Call Option on stock,所以它具有股票和债券的双重属性。

至于这个Convertible bond什么时候更像债券,什么时候更像股票,就看这个Call option on stock的价值了。大体来讲,当option是Out of the money,可转债更像是债券,此时债券的收益就决定了可转债的收益;当option是in the money,可转债是更像股票,此时可转债的价格变动基本上就受股票价格变动的支配了,当Option是in-the-money的时候,可转债的价值变动基本上就是和股票1:1的变动了。

文中对股价的预测是:Raffarin's share price will appreciate toward the conversion price but not exceed it。

当标的股票的价格更靠近Converision price,但没有超过。意味着Option的价值在增加;但是由于还没有到行权价,这个option并不能1:1的反应股票价格变动,由于不能行权,Option价值增加要小于股票价值增加,所以可转债的收益增加小于对应股票收益的增加。

总结一下本题,当标的股票的价格增加时,Option的价值增加,由于convertible bond的价值等于一个straight bond + Call option on stock,所以此时可转债的价值是增加的。但是Option还没有到行权价,可转债还不能转成股票、而option的价值增长小于股票的价值增长,所以可转债的增长幅度要小于股票的增长幅度。

讲义中相关的内容:

NO.PZ201712110200000409 问题如下 Baseon Exhibit 4 anGillette’s forecast regarng Raffarin’s share price, the return on the RI bonover the next yeis most likely to be: A.lower ththe return on Raffarin’s common shares. B.the same the return on Raffarin’s common shares. C.higher ththe return on Raffarin’s common shares. A is correct.Over the next year, Gillette believes thRaffarin’s share priwill continue to increase towar the conversion pribut not exceeit. If Gillette’s forecast becomes true, the return on the RI bonwill increase but a lower rate ththe increase in Raffarin’s share pribecause the conversion priis not expecteto reache 视频讲解中提到,当股票价格向转换价格靠近时,可转债股性债性并存,处于一个涨跌幅均小于正股的情况,这个我可以理解。那如果题目问可转债当前out of money,正股价格预计继续下降,债相关的利率因素等不变,可转债价格应当如何变化?假设答案给了【A.可转债价格会下降但幅度更小】【B.可转债价格不变】。这种情况下应该怎么选择?是用“可转债out of money时偏债性,只受利率影响”的结论去选择B,还是用“可转债涨跌幅小于正股”的大原则去选择A?还请老师解惑。

NO.PZ201712110200000409问题如下Baseon Exhibit 4 anGillette’s forecast regarng Raffarin’s share price, the return on the RI bonover the next yeis most likely to be:A.lower ththe return on Raffarin’s common shares.B.the same the return on Raffarin’s common shares.C.higher ththe return on Raffarin’s common shares.A is correct.Over the next year, Gillette believes thRaffarin’s share priwill continue to increase towar the conversion pribut not exceeit. If Gillette’s forecast becomes true, the return on the RI bonwill increase but a lower rate ththe increase in Raffarin’s share pribecause the conversion priis not expecteto reache老师,我想确认一下,这边说的return 是指,如果可转债以债券形式持有的话,拿到的就是债券的收益, 比如,coupon 或者是利息收入; 如说是转为股票持有,就是拿到的 分红收益 或者是 capitgain 的收益 对吗?

老师如果这道题是股票价格下降,并远离conversion price,那是不是可转债的return就要大于stoprireturn了?因为这时候的可转债的return基本可以当做是straight bon价格变化,变化很小,可以认为股票下跌的要多于这个变化,就像这道题一样,对吗?

the same the return on Raffarin’s common shares. higher ththe return on Raffarin’s common shares. A is correct. Over the next year, Gillette believes thRaffarin’s share priwill continue to increase towar the conversion pribut not exceeit. If Gillette’s forecast becomes true, the return on the RI bonwill increase but a lower rate ththe increase in Raffarin’s share pribecause the conversion priis not expecteto reache老师请问,这里convertible bonreturn比标的storeturn难道不是因为可转债有premium吗?

你好,为什么不用综合考虑RI bonconvertible callable putable这三个性质呢?谢谢!