NO.PZ2019120301000067

问题如下:

Question

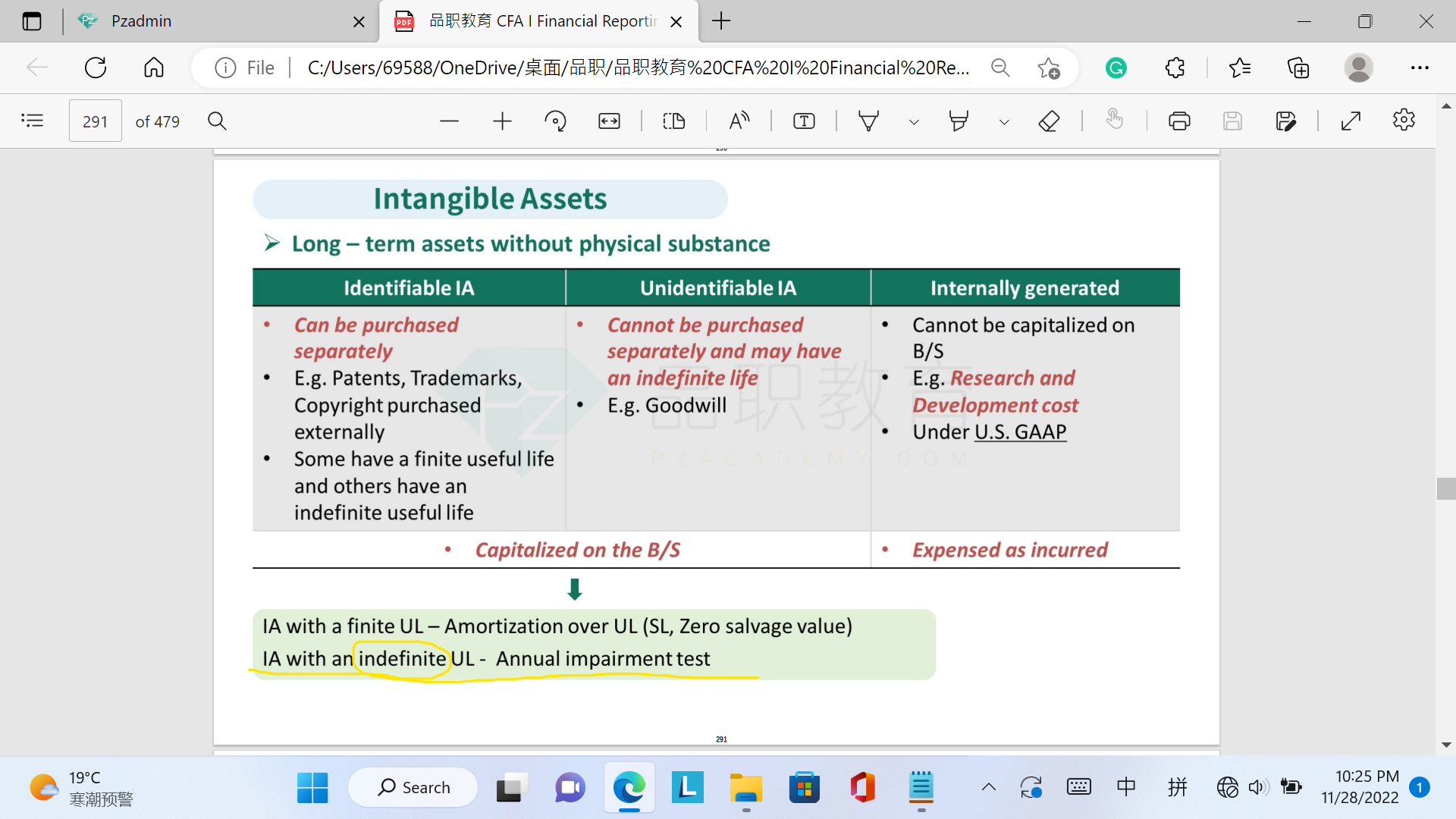

It purchased a customer list for $100,000, which is expected to provide equal annual benefits for the next four years.

It recorded $200,000 of goodwill in the acquisition of a competitor. It is estimated that the acquisition would provide substantial benefits for the company for at least the next 10 years.

It spent $300,000 on media placements announcing that the company had donated products and services to the community. The CEO believes the firm’s reputation was enhanced substantially and that the company will likely benefit from it for the next five years.

Based on those events occurred at a company during 2013, the amortization expense that the company should report in 2014 is closest to:

选项:

A.$85,000.00 B.$25,000.00 C.$45,000.00解释:

SolutionB is correct. The customer list is the only identifiable intangible asset, and it should be amortized on a straight-line basis over its expected future life: $100,000/4 = $25,000/year. Goodwill is an unidentifiable intangible and should be tested for impairment but not amortized. All advertising and promotion costs, such as the media placements, are typically expensed. If the reputation of the company has been enhanced as the CEO suggests, it is an internally generated intangible that is not recorded on the balance sheet and is thus not amortized.

A is incorrect. It includes the $300,000 of donation amortized over 5 years (300,000/5 = 60,000) added to the customer list amortization: 25,000 + 60,000 = 85,000.

C is incorrect. It amortizes the goodwill over 10 years and adds it to the $25,000 amortization of the customer list: $200,000/10 + $100,000/4 = $45,000.

老师,我前面问错了,想问下C项是属于intangible infinite嘛?不用摊销,所以费用化?