NO.PZ2022061303000021

问题如下:

An inverse floater will most likely have:

选项:

A.a maximum coupon rate.

B.a face value that changes as the reference rate changes.

C.a coupon rate that changes by more than the change in the reference rate.

解释:

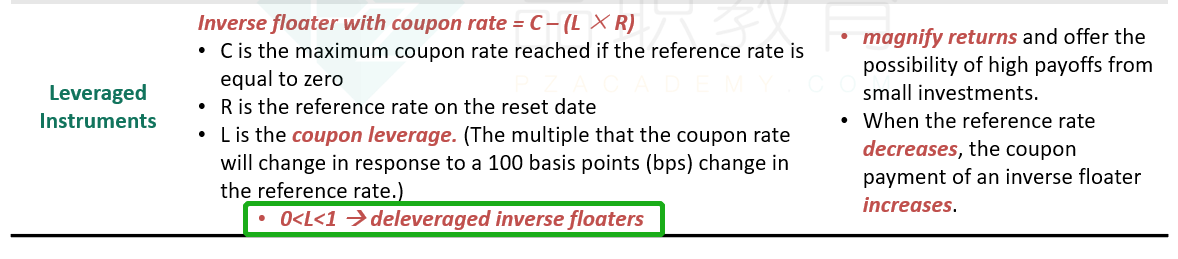

A is correct. The general formula for the coupon rate of an inverse floater is C – (L × R), where C is the maximum coupon rate if the reference rate (R) is equal to zero and L is the coupon leverage, which is greater than zero.

B is incorrect. The face value of an inverse floater does not change as the reference rate changes; rather, the coupon rate changes.

C is incorrect. Inverse floaters can have leverage less than 1 (deleveraged inverse floaters), so the coupon rate changes by less than the change in the reference rate; leverage greater than 1 (leveraged inverse floaters), so the coupon rate changes by more than the change in the reference rate; or leverage equal to 1, so the coupon rate changes by the same amount as the change in the reference rate.

考点:反向浮动债券

解析:反向浮动债券,其票面利率的一般公式是C - (L × R)。票面利率会随着参考利率的变化而变化,而非面值。当参考利率R等于零时,C是最大票面利率,L是大于零的票面杠杆率。

为什么反向浮动会有一个最大的reference rate啊

拿老师讲的例子

coupon rate=7%-MRR 这怎么看出有最大的MRR啊

reference rate不就是公式里的MRR吗