NO.PZ2016012101000138

问题如下:

Eric’s Used Book Store prepares its financial statements in accordance with IFRS. Inventory was purchased for £1 million and later marked down to £550,000. One of the books, however, was later discovered to be a rare collectible item, and the inventory is now worth an estimated £3 million. The inventory is most likely reported on the balance sheet at:

选项:

A.£550,000.

B.£1,000,000.

C.£3,000,000.

解释:

B is correct.

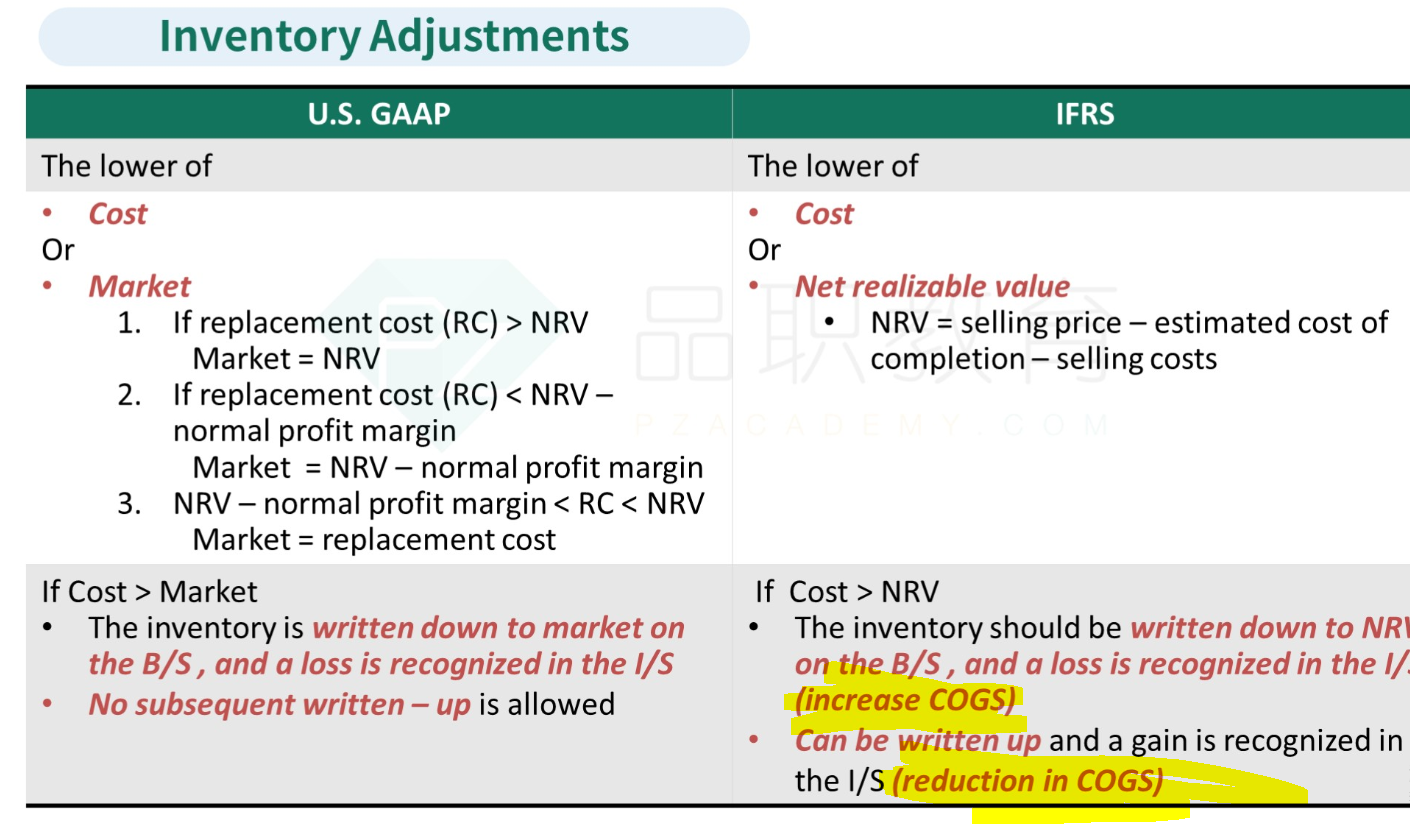

Under IFRS, the reversal of write-downs is required if net realisable value increases. The inventory will be reported on the balance sheet at £1,000,000. The inventory is reported at the lower of cost or net realisable value. Under US GAAP, inventory is carried at the lower of cost or market value. After a write-down, a new cost basis is determined and additional revisions may only reduce the value further. The reversal of write-downs is not permitted.

解析:国际准则下,减值损失可以回转,但又不能超过Cost。现在存货价值3million,cost=1million,所以只能回转到1million。

rt