NO.PZ2016071602000022

问题如下:

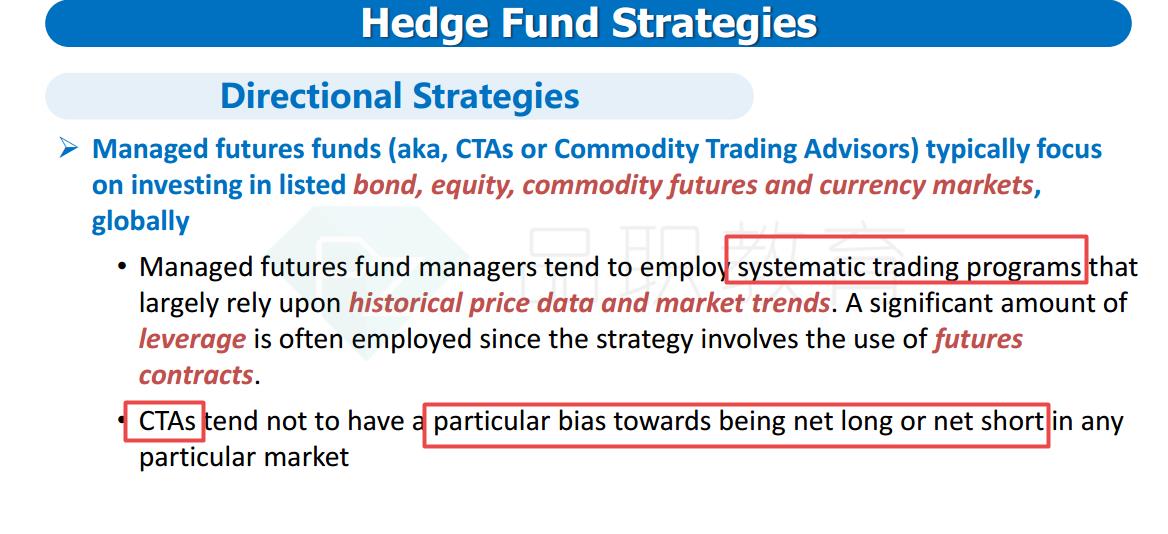

The Big Bucks hedge fund has the following description of its activities. It uses simultaneous long and short positions in equity with a net beta close to zero. Which of the following statements about Big Bucks is/are correct?

I. It uses a directional strategy.

II. It is a relative value hedge fund.

III. This fund is exposed to idiosyncratic risks.

选项:

A.I and II

B.II and III

C.I and III

D.II only

解释:

B is correct. This fund has zero beta, so is a relative value fund. It is, however, exposed to idiosyncratic, stock-specific risk.

relative value fund老师相对价值策略不是A股票相对于B股票价格便宜,所以longA,shortB,这里针对同一只股票即long又short,也叫relative 策略?