Assume that the one-year probabilities of

default for the AAA- and BBB-rated bonds are 1% and 4%, respectively, and the joint probability of default of the two bonds is 0.07%. What is the default

correlation between the two bonds?

选项:

A.

0.03%

B.

1.54%

C.

78.91%

D.

The

default correlation cannot be calculated with the information provided.

解释:

B is correct.

考点:Default Correlation

解析:

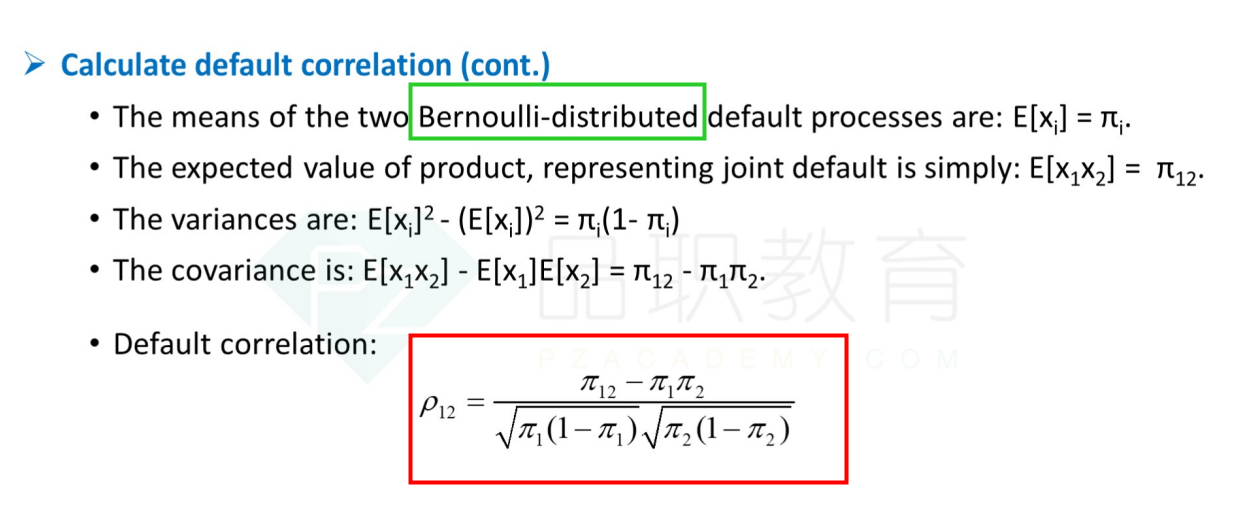

From Equation:p(A and B)=Corr(A,B)p(A)[1−p(A)]×p(B)[1−p(B)]+p(A)p(B), the default correlation isCorr(A,B)=p(A)[1−p(A)]×p(B)[1−p(B)]p(A and B)−p(A)p(B)=0.01×(1−0.01)0.04×(1−0.04)0.0007−0.01×0.04=0.0154.

题目是否还需要说明 AAA- and BBB-rated bonds的违约概率均满足Bernoulli分布?