开发者:上海品职教育科技有限公司 隐私政策详情

应用版本:4.2.11(IOS)|3.2.5(安卓)APP下载

随时随地学习课程,支持音视频下载!

Shelly · 2022年10月18日

No.PZ2020021002000100 (选择题)

来源: 原版书

If fund A is mean-variance inefficient in relation to fund B, then fund B is expected to outperform fund A according to SPI

答案: true

疑问: 从mean-variance inefficent 具体指的是什么?是指sharp ratio吗?

品职答疑小助手雍 · 2022年10月19日

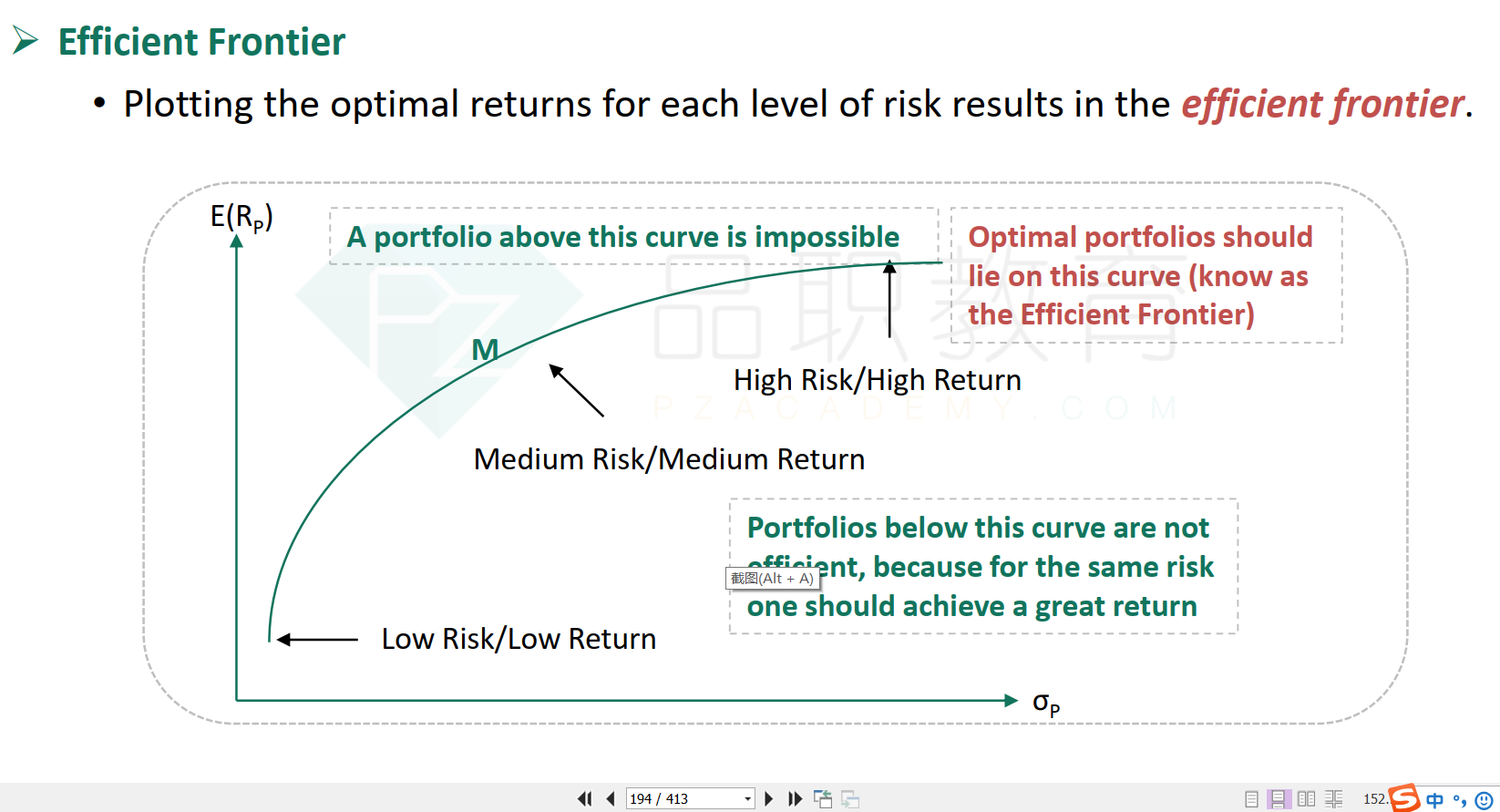

同学你好,这个要看对知识点的敏感性了,看到mean-variance inefficient就要想到下面这张图~

因为fundA不efficient,所以它相对fundB在CML线以下,也就意味着从rf发出的斜线斜率比B低,所以A的SPI低

Shelly · 2022年10月20日

了解了,谢谢老师~