NO.PZ2020042003000087

问题如下:

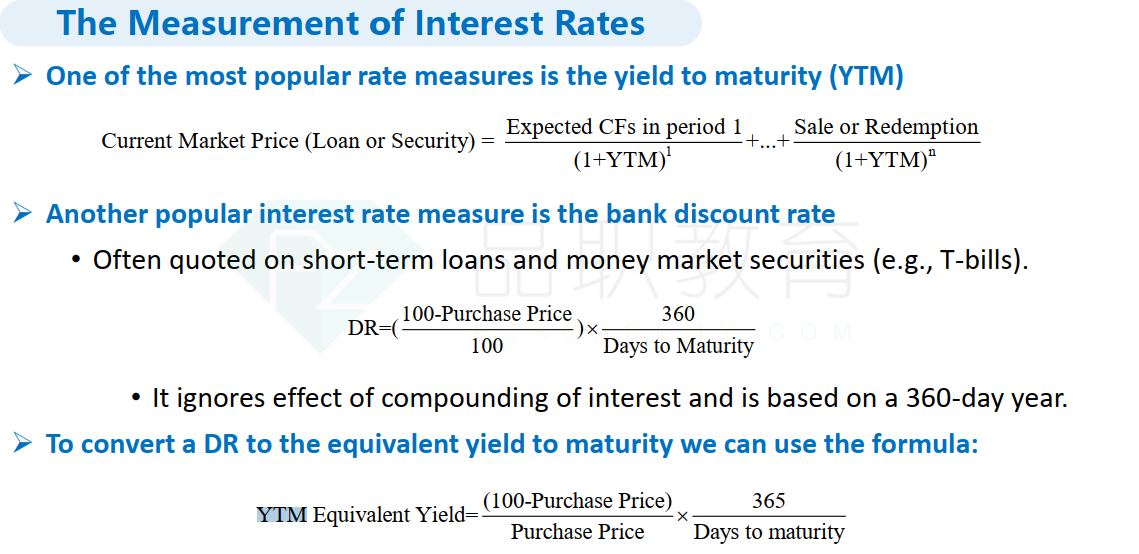

The price of a 30-day T-bill is 99.5, what is

the discount rate?

选项:

A. 6%

2%

3%

4%

解释:

考点:对Risk Management for Changing Interest

Rates: ALM and Duration Techniques- Interest Rate Risk的理解

答案:A

解析:

DR = (100 – Purchase price)/100 × 360/Days to maturity = (100 – 99.5)/100 × 360/30

= 6%

这道题是用360算的,

为什么 No.PZ2020042003000088 这道用365?