NO.PZ2018070201000092

问题如下:

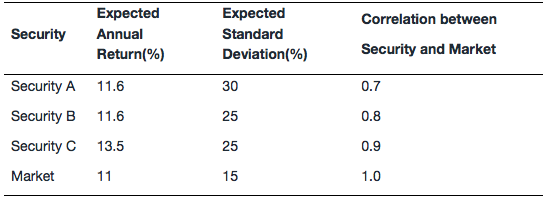

Tim, an analyst of an investment company forecasts the return and deviation of below securities. Based on these information, which statement is most correct:

选项:

A.Security A has the highest total risk.

B.

Security B has the highest total risk.

C.Security C has the highest total risk.

解释:

A is correct.

The total variance of security A is =0.09

The total variance of security B is =0.0625

The total variance of security C is =0.0625

The total variance of A >The total variance of B =The total variance of C.

Security A has the highest total risk.

题目问的是Total risk,那应该跟资产与市场的敏感性有关,为什么beta在这里是无效信息?为什么不能说beta越大,资产波动性越大,也即risk越大?