NO.PZ2018070201000062

问题如下:

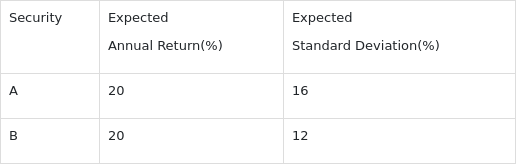

Laurel, an manager from an investment company, recently constructs the following portfolio, assuming that the two assets are not relevant, what is the expected standard deviation if the two assets are equal-weighted:

选项:

A.8.00%.

B.10.00%.

C.12.00%.

解释:

Each stock contains the same weight in the equal-weighted portfolio, so

这道题correlation/covariance为什么用了0?

题干说not relevant,not relevant不应该是-1吗?完全不相关?前面有道题也说了“当相关系数为0的时候,可以构建一个零方差组合。是不对的,只有当相关系数为-1的时候,也就是他们完全负相关,构建的投资组合才是零方差的。”