NO.PZ2016010801000115

问题如下:

In spot market, Swiss Franc (CHF) is traded at CHF/EUR 1.1613. In forward market, the 90-day forward rate is CHF/EUR 1.1592. Which of the following statement is most likely correct?

选项:

A.Interest rates are lower in the Euro Zone relative to Switzerland.

B.Interest rates are higher in the Euro Zone relative to Switzerland.

C.More CHF is needed to exchange one EUR in the forward market than exchange in the spot market.

解释:

B is correct.

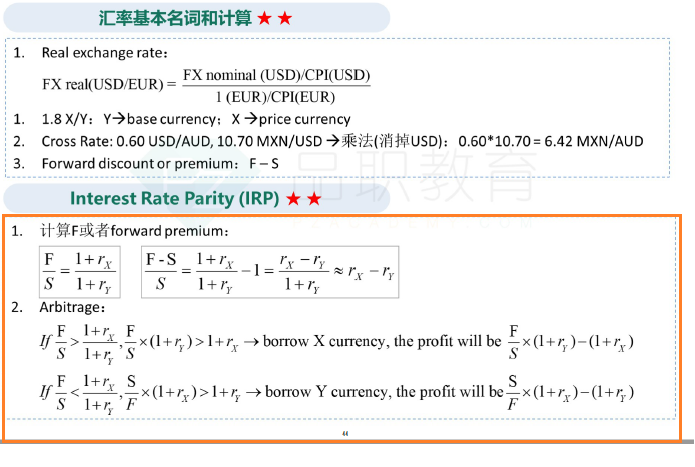

Forward rate in CHF/EUR = spot rate* (1+interest rate in Switzerland)/(1+interest rate in Euro Zone). Forward rate is lower than spot rate in CHF/EUR as1.1592<1.1613, therefore Interest rates are higher in the Euro Zone than in Switzerland.

考点:Forward rate

解析:瑞士法郎/欧元远期利率=即期利率*(1+瑞士利率)/(1+欧元区利率)。远期利率低于即期汇率(CHF/EUR =1.1592<1.1613),因此欧元区利率高于瑞士区利率。

作为price的货币利率高,远期的汇率就会升高

作为base的货币利率高,远期的汇率就会降低

price的货币利率高,钱应该会从base货币的国家流向price货币的国家啊,应该会升值才对啊?

就像现在美国利率高,美元就在升值;

这道题Euro的利率高了,1 Euro兑的CHF反而降低了,为什么?