老师,我想问一下C问:2y/5y/10y/30y期的yield curve 变化分别为 +0.35%/+0.2%/不变/ -0.35%。短期利率上升,price下降(应该减少Duration);长期利率下降,price上升(应该增加duration)。我知道本题的考点是“bullet vs ladder vs barbell”。如果选择barbell,barbell在2y和30y的权重不一样(2y的占比62.45%,比30y(37.55%)高很多。)我不是很理解的是:选barbell之后,2y的duration是不是也会增加(会产生负面影响)?而且2y的占比超过30y的占比(所以,这个barbell实际上是不是更接近于一个偏短期的bond)?不过这道题目数字也不全,无法定量计算。请问老师,C问在对比“bullet vs ladder vs barbell”时候,应该从哪个角度思考?

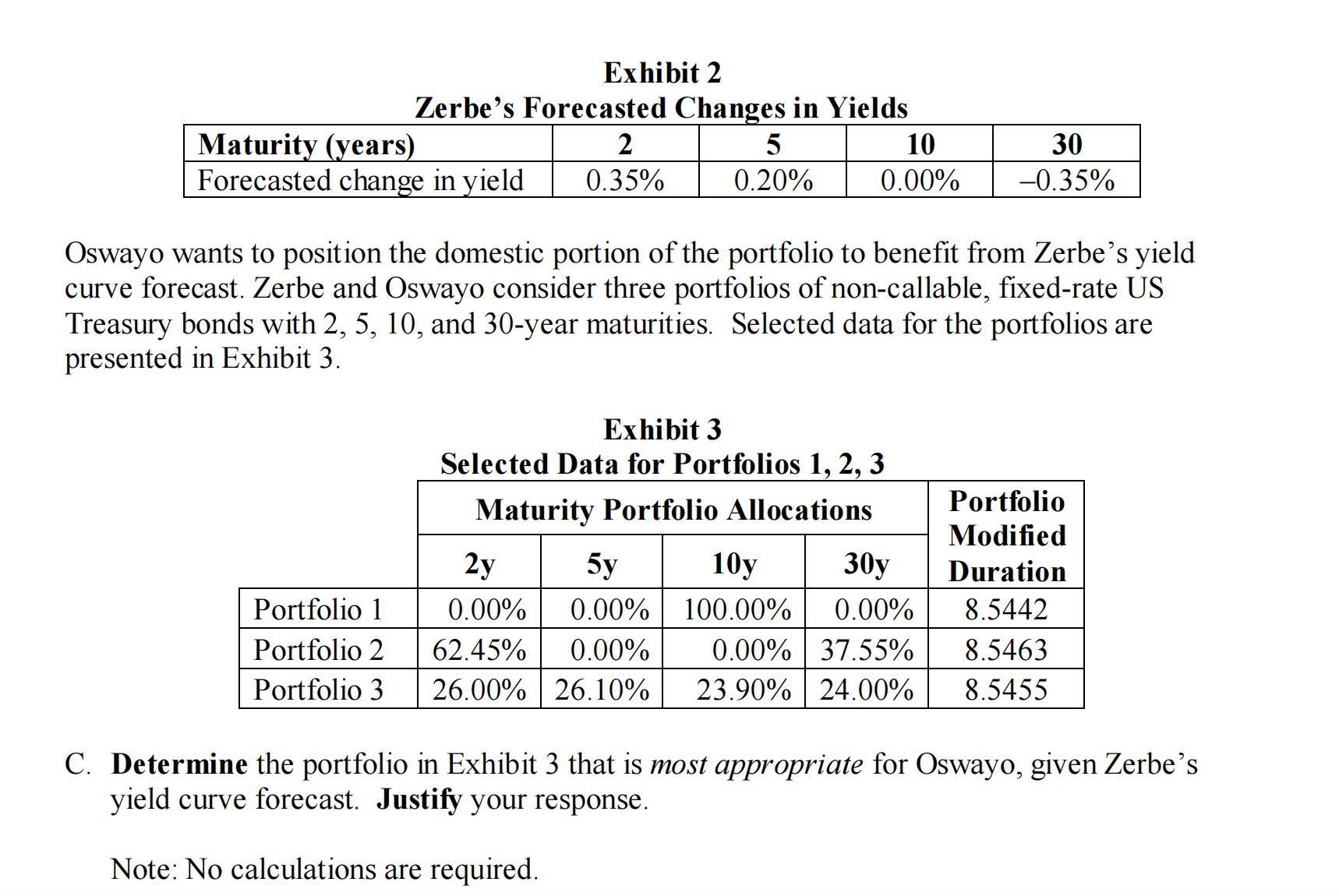

答案:Portfolio 2.

The most appropriate portfolio is Portfolio 2. Barbell portfolios—combining securities concentrated in short and

long maturities, as in Portfolio 2—are typically used to take advantage of a flattening yield curve. Zerbe expects

the yield curve to flatten, with the twist pinned at the 10-year yield. That means the 10-year yield will remain

unchanged, while the 2-year and 5-year yields will increase, and the 30-year yield will decrease.

Although all three portfolios have similar modified durations, and therefore approximately the same change in

value for a parallel shift in the yield curve, the impact of Zerbe’s forecasted yield curve flattening will be most

advantageous for the barbell (Portfolio 2) and least advantageous for the bullet (Portfolio 1), with the ladder

(Portfolio 3) in the middle.

The only yield that falls, thereby creating a price increase, is that of the 30-year bond. Portfolio 2 benefits most

from the drop in the 30-year yield, while Portfolio 3 benefits less because of its smaller allocation to the 30-year

bond, and Portfolio 1 doesn’t benefit at all because it doesn’t hold any of the 30-year bond. For Portfolio 2, even

though the 2-year and 30-year yields change by the same absolute magnitude, the price impact on the 30-year bond

will be much larger than on the 2-year because the duration of the 30-year bond is much larger than that of the 2-

year bond.

Since the forecasted twist is pinned at the 10-year yield, the 10-year yield will not change; therefore, there is no

price impact on Portfolio 1 from this forecasted curve twist. Portfolio 3 will underperform Portfolio 2 for this yield

curve flattening, as it holds a smaller position in the 30-year bond, giving it less price increase than Portfolio 2.

Portfolio 3 also holds a larger position in the 5-year bond, which will cause some price decrease with the increase

in the 5-year yield.