NO.PZ202108100100000201

问题如下:

Based on Exhibit 1, Johnson should price the three-year Libor-based interest rate swap at a fixed rate closest to:

选项:

A.0.34%.

1.16%.

1.19%.

解释:

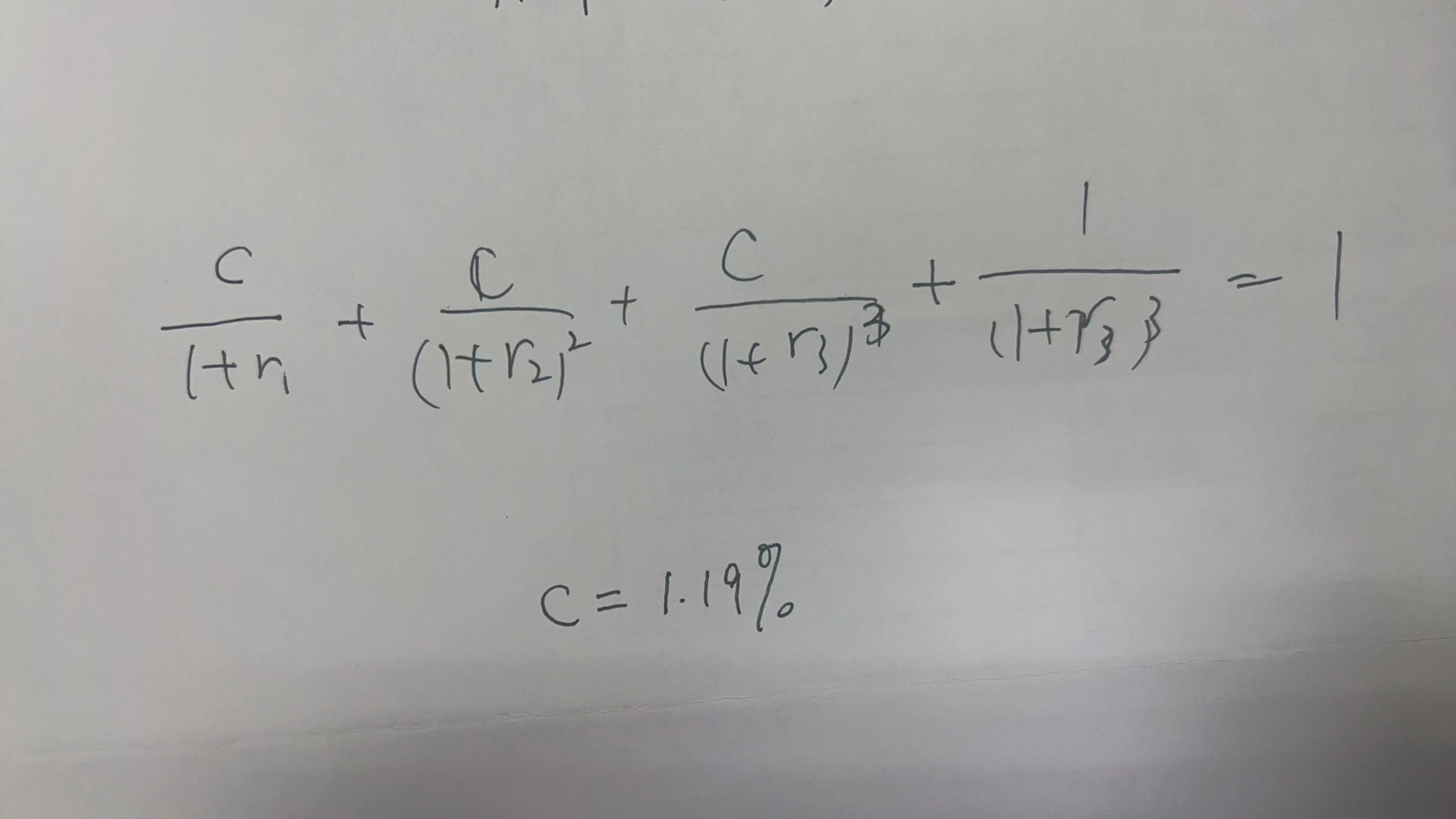

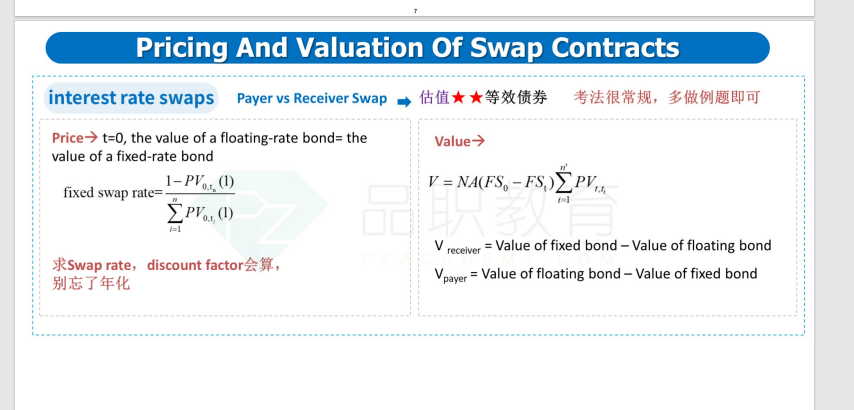

C is correct. The swap pricing equation is

That is, the fixed swap rate is equal to 1 minus the final present value factor (in this case, Year 3) divided by the sum of the present values (in this case, the sum of Years 1, 2, and 3). The sum of present values for Years 1, 2, and 3 is calculated as

Thus, the fixed-swap rate is calculated as

中文解析:

本题考察的是对利率互换进行定价。

题干已经给到了折现因子,直接带入公式:计算即可。

注意本题中是每年互换一次,因此根据公式求得结果不需要进行年化处理。

这考的是哪个考点呢?上课好像都没接触过啊