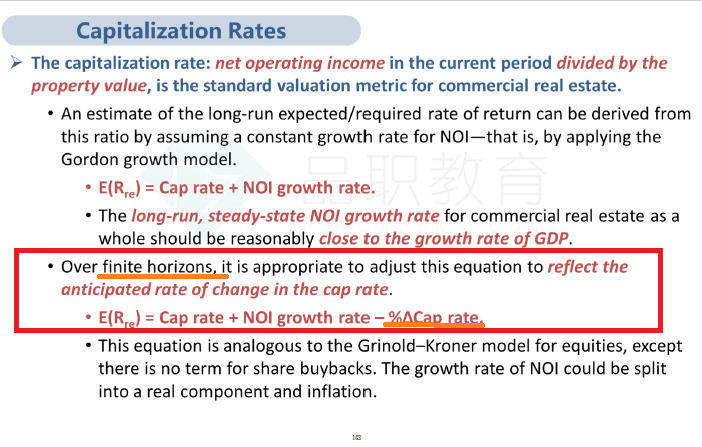

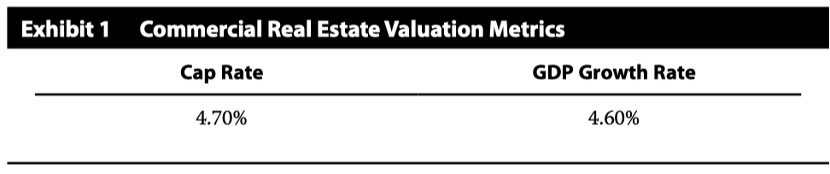

Martin looks over the long-run valuation metrics the manager is using for commercial real estate, shown in Exhibit 1.

The real estate team uses an in-house model for private real estate to estimate the true volatility of returns over time. The model assumes that the current observed return equals the weighted average of the current true return and the previous observed return. Because the true return is not observable, the model assumes a relationship between true returns and observable REIT index returns; therefore, it uses REIT index returns as proxies for both the unobservable current true return and the previous observed return.

(1)Based only on Exhibit 1, the long-run expected return for commercial real estate:

A is approximately double the cap rate.

B incorporates a cap rate greater than the discount rate.

C needs to include the cap rate’s anticipated rate of change.

答案A