NO.PZ202201040100000102

问题如下:

Berger isconcerned about possible financial difficulties for the surviving spouse in theevent of the other’s premature death. He advises the Josephs to considermitigating this risk by purchasing life insurance policies.

Berger suggests using theneeds analysis method to determine the required insurance amount. He firstestimates cash needs for Jennifer and Ron and then estimates that the survivingspouse would live until age 85 and require $35,000 annually for livingexpenses, and that those expenses would increase 2% annually in nominal terms.He assumes a 2.5% discount rate. Berger also estimates the present value of thesurviving spouse’s salary income until retirement at age 65 for both Jenniferand Ron. Exhibit 1 presents an abbreviated life insurance worksheet.

Calculate the amount of life insurance needs for bothJennifer and Ron individually, based on Berger’s assumptions and Exhibit 1.

解释:

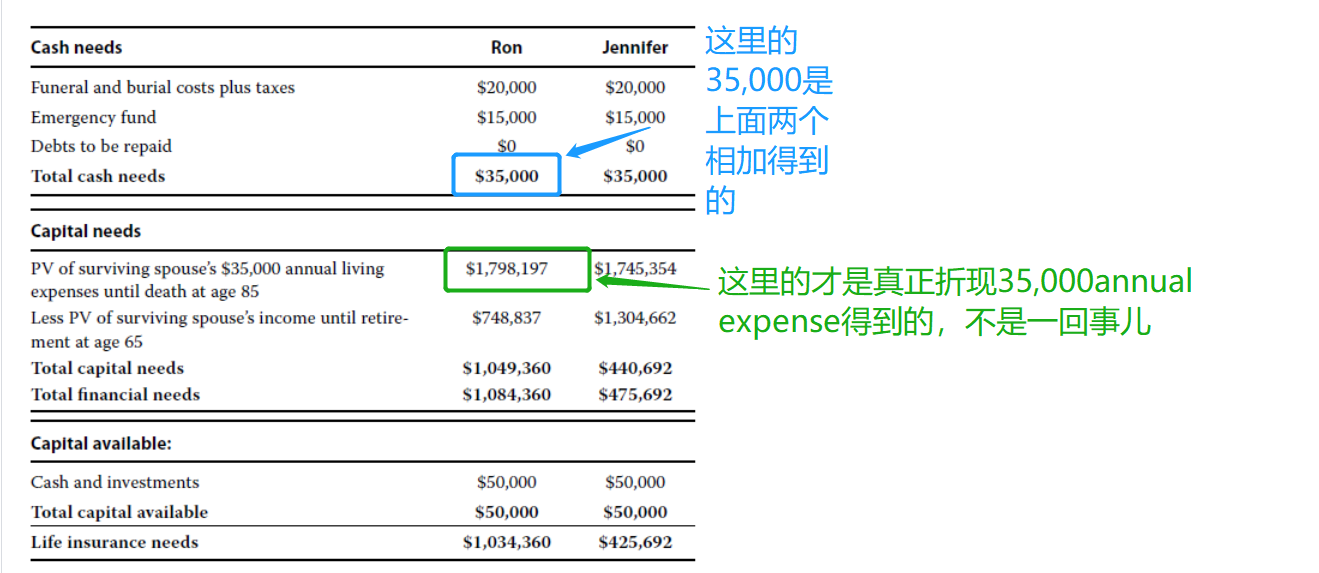

The needs analysis method determines the amount of life insurance required by estimating the amount needed to cover the surviving spouse’s annual living expenses. It is calculated as the difference between the family’s total financial needs (total cash needs plus total capital needs) and total capital available. The amount of life insurance coverage that the Josephs require is calculated as follows:

The present value of the surviving spouse’s annual living expenses of $35,000 until death at age 85 is determined as the present value of an annuity due. Growth in expenses is incorporated into the calculations by adjusting the discount rate to account for the growth in expenses. The adjusted discount rate is calculated as [(1 + Discount Rate)/(1 + Growth Rate in Expenses)] – 1.

The present value of the surviving spouse’s annual living expenses of $35,000 until death at age 85 for Jennifer (n = 59) in the case of Ron’s death is calculated as follows:

First, adjust the discount rate to account for the growth rate:

Adjusted Discount Rate = (1.025/1.02) – 1 = 0.4902% (rounded up)

Now, setting the calculator for beginning-of - period payments, compute the PV:

n = 59

I/Y = 0.4902

PMT = $35,000

CPT PV = $1,798,197

Similarly, the present value of the surviving spouse’s annual living expenses of $35,000 until death at age 85 for Ron (n = 57) in the case of Jennifer’s death is calculated as follows:

Again, setting the calculator for beginning-of - period payments, compute the PV:

n = 57

I/Y = 0.4902

PMT = $35,000

CPT PV = $1,745,354

The Josephs’ additional life insurance needs aresummarized in the following table:

Based on the needs analysis method, the Josephs should purchase life insurance policies in the amounts of $1,034,360 and $425,692 on Ron and Jennifer, respectively.

需求分析法通过估计支付未亡配偶每年生活费用所需的金额来确定所需的人寿保险金额。它的计算方法是家庭总财务需求(总现金需求加上总资本需求)与可用总资本之间的差额。约瑟夫夫妇要求的人寿保险金额计算如下:

尚存配偶每年 35,000 美元直至 85 岁去世的生活费用的现值被确定为到期年金的现值。通过调整贴现率以考虑费用的增长,将费用的增长纳入计算。调整后的贴现率计算为 [(1 + 贴现率)/(1 + 费用增长率)] – 1。

在罗恩去世的情况下,珍妮弗 (n = 59) 在 85 岁时去世前尚存配偶每年生活费用 35,000 美元的现值计算如下:

首先,调整贴现率以考虑增长率:

调整后贴现率 = (1.025/1.02) – 1 = 0.4902%(向上取整)

现在,设置期初付款的计算器,计算 PV:

n = 59

I/Y = 0.4902

PMT = 35,000 美元

CPT PV = $1,798,197

同样,在詹妮弗去世的情况下,罗恩 (n = 57) 在 85 岁时去世前尚存配偶每年生活费用 35,000 美元的现值计算如下:

同样,设置期初付款的计算器,计算 PV:

n = 57

I/Y = 0.4902

PMT = 35,000 美元

CPT PV = $1,745,354

下表总结了约瑟夫一家的额外人寿保险需求:

根据需求分析方法,约瑟夫一家应该分别为 Ron 和 Jennifer 购买金额为 1,034,360 美元和 425,692 美元的人寿保险单。

35000折现计算了一次,购物欲又加了一个35000,这是否是重复计算了?