NO.PZ2018070201000093

问题如下:

Tim, an analyst of an investment company forecasts the return and deviation of below securities. Based on these information, which statement is most correct:

选项:

A.Security A has the highest beta value.

B.Security B has the highest beta value.

C.Security C has the highest beta value.

解释:

C is correct.

The beta value of security A is1.4

The beta value of security B is 1.33

The beta value of security C is1.5

Security C has the highest beta value.

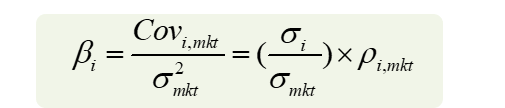

老师,能不能用中文把这个公式的原型和变形验算一下,感觉贝塔有很多变形,但我并没有掌握到精髓