NO.PZ201812020100000104

问题如下:

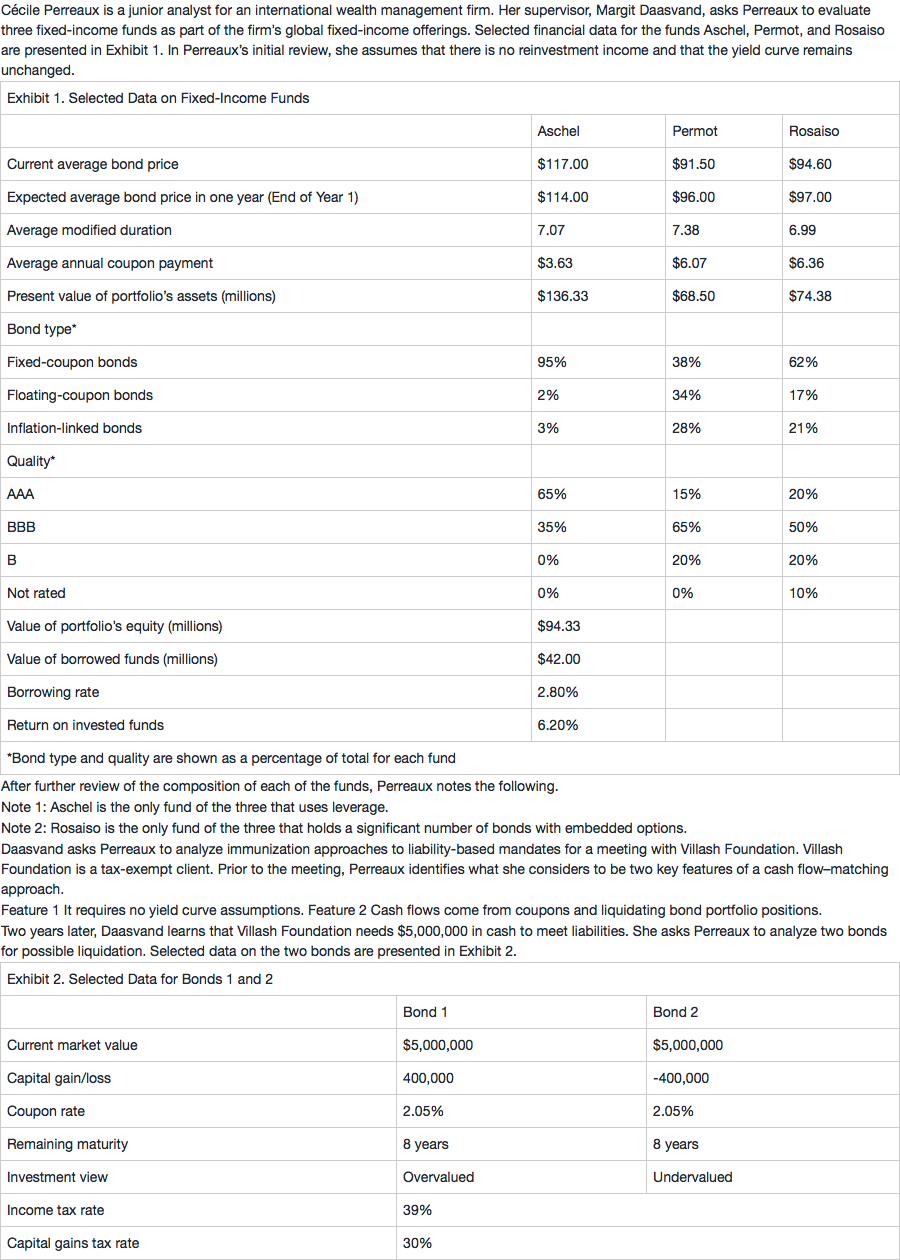

Based on Note 2, Rosaiso is the only fund for which the expected change in price based on the investor’s views of yields and yield spreads should be calculated using:

选项:

A.convexity.

B.modified duration.

C.effective duration

解释:

C is correct.

Rosaiso is the only fund that holds bonds with embedded options. Effective duration should be used for bonds with embedded options. For bonds with embedded options, the duration and convexity measures used to calculate the expected change in price based on the investors’s views of yields and yield spreads are effective duration and effective convexity. For bonds without embedded options, convexity and modified duration are used in this calculation.

题目问的是based on the investor’s views of yields and yield spreads。而题干中investor' view是yield不变。那么如果是平移,用effective duration衡量,非平移用effective convexity来衡量,对吧?