NO.PZ2018070201000062

问题如下:

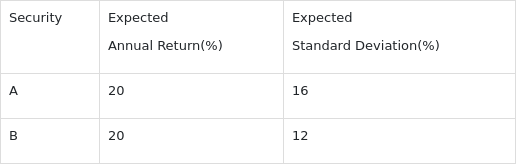

Laurel, an manager from an investment company, recently constructs the following portfolio, assuming that the two assets are not relevant, what is the expected standard deviation if the two assets are equal-weighted:

选项:

A.8.00%.

B.10.00%.

C.12.00%.

解释:

Each stock contains the same weight in the equal-weighted portfolio, so

不是=w1^2SIGMA1^2+W2^2SIgMA^2+2w1w2sigma1sigma2P12吗