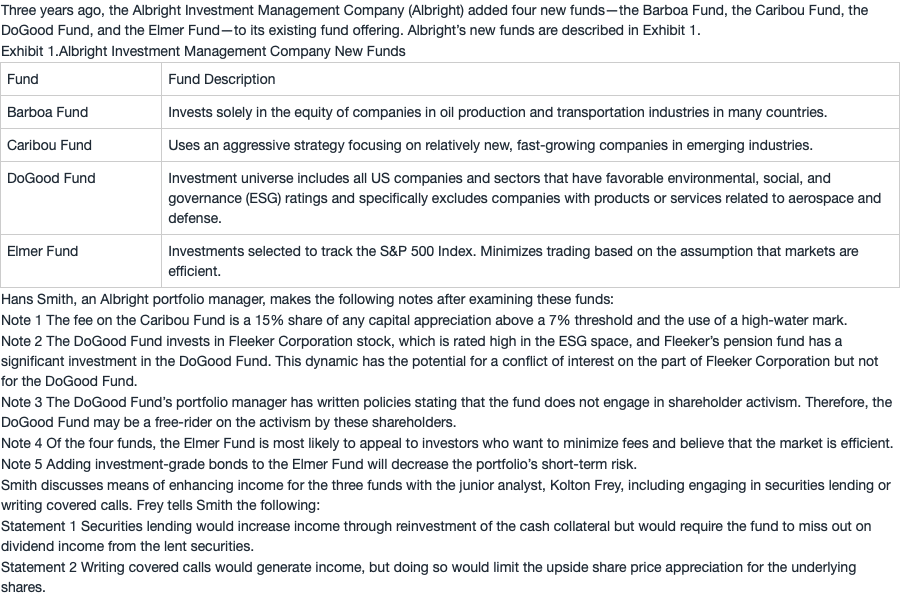

NO.PZ201809170400000104

问题如下:

The Elmer fund’s management strategy is:

选项:

A.active.

B.passive.

C.blended.

解释:

B is correct. The fund is managed assuming that the market is efficient, and investments are selected to mimic an index. Compared with active strategies, passive strategies generally have lower turnover and generate a higher percentage of long-term gains. An index fund that replicates its benchmark can have minimal rebalancing.

其实equity那里不是有4 个universe吗:style&size, geograhy, activity和index. 按照老师的思路,其实这4个即可active又可以passive。不知道是否正确。