NO.PZ202108100100000304

问题如下:

he value of the JGB long forward position is closest to:

选项:

A.JPY15,980,823.

JPY15,990,409.

JPY16,000,000

解释:

B is correct.

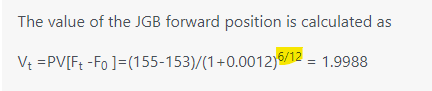

The value of the JGB forward position is calculated as

Vt =PV[Ft -F0 ]=(155-153)/(1+0.0012)6/12 = 1.9988

Therefore, the value of the long forward position is 1.9988 per JPY100 par value.

For the long position in eight contracts with each contract having a par value of

100 million yen, the value of the position is calculated as

0.019988 × (JPY100,000,000) × 8 = JPY15,990,409.

中文解析:

本题考察的是使用重新定价法来计算远期合约的价值。

当题目直接给到0时刻和t时刻的远期合约的价格时,即是暗示我们可以直接按照公式Vt =PV[Ft -F0 ]计算即可。

需要注意两点:

1. 合约报价是以100为基础进行报价的,我们需要换算为对应的名义本金为100million,因此需要先对1.9988除以100然后再乘以100 million

2. 注意合约份数是8份,因此最后需要乘以8.

0.12%这个为什么不去年化乘以0.5呢