老师好 R13 课后题 第一题

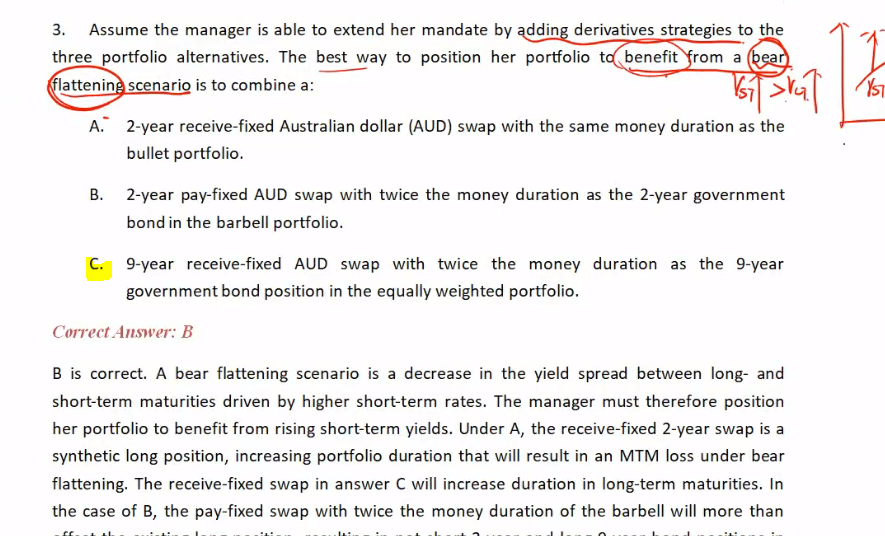

1) bear flattening 不是 是 要short ST, long LT, 然后是NET negative duration 吗? 为啥这里老师说一看到Long LT 是增加duration, C 就不用考虑了?

2) short ST, long LT, 要得到negative duration 不就是 short term's duration 大于 long term duration , 这里正好短期变动幅度大于长期变动幅度, 所以 D short term > D long term, short st, long LT 就是 - D short term + D long term = 总的D 是负的, 这样理解对吗? 谢谢。