NO.PZ2016072602000057

问题如下:

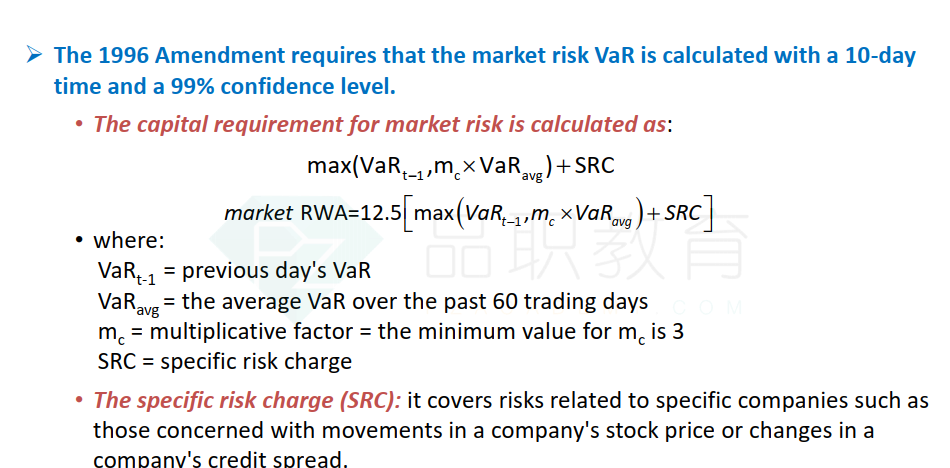

Under the 1996 market risk amendment to the Basel Accord, a bank can use its internal models to calculate its market risk charge subject to all the following provisions except:

选项: A time horizon of 10 trading days

A 99% confidence level

C.One year of historical observations, which are updated semiannually

D.The market risk charge set at the higher of the previous day’s VAR or the average VAR over the past 60 days scaled by a multiplicative factor

解释:

C is correct. The IMA requires using one year of historical data updated at least quarterly, not semiannually.

本题描述的是1996巴一不遵循哪个条款,因D是2.5的条款,所以我的理解是选D,不用被遵循。