NO.PZ201809170400000606

问题如下:

Which of Garcia’s statements regarding investing with long–short and long-only managers is correct?

选项:

A.

Only Statement 1

B.

Only Statement 2

C.

Both Statement 1 and Statement 2

解释:

C is correct. Both Statement 1 and Statement 2 are correct.

Statement 1 is correct because, similar to a long-only portfolio, a long–short portfolio can be structured to have a gross exposure of 100%. Gross exposure of the portfolio is calculated as the sum of the long positions and the absolute value of the short positions, expressed as percentages of the portfolio’s capital.

Gross exposure = Long positions + |Short positions|

Gross exposure long-only portfolio = 100% (Long positions) + 0% (Short positions) = 100%

Gross exposure long–short portfolio = 50% (Long positions) + |–50%| (Short positions) = 100%

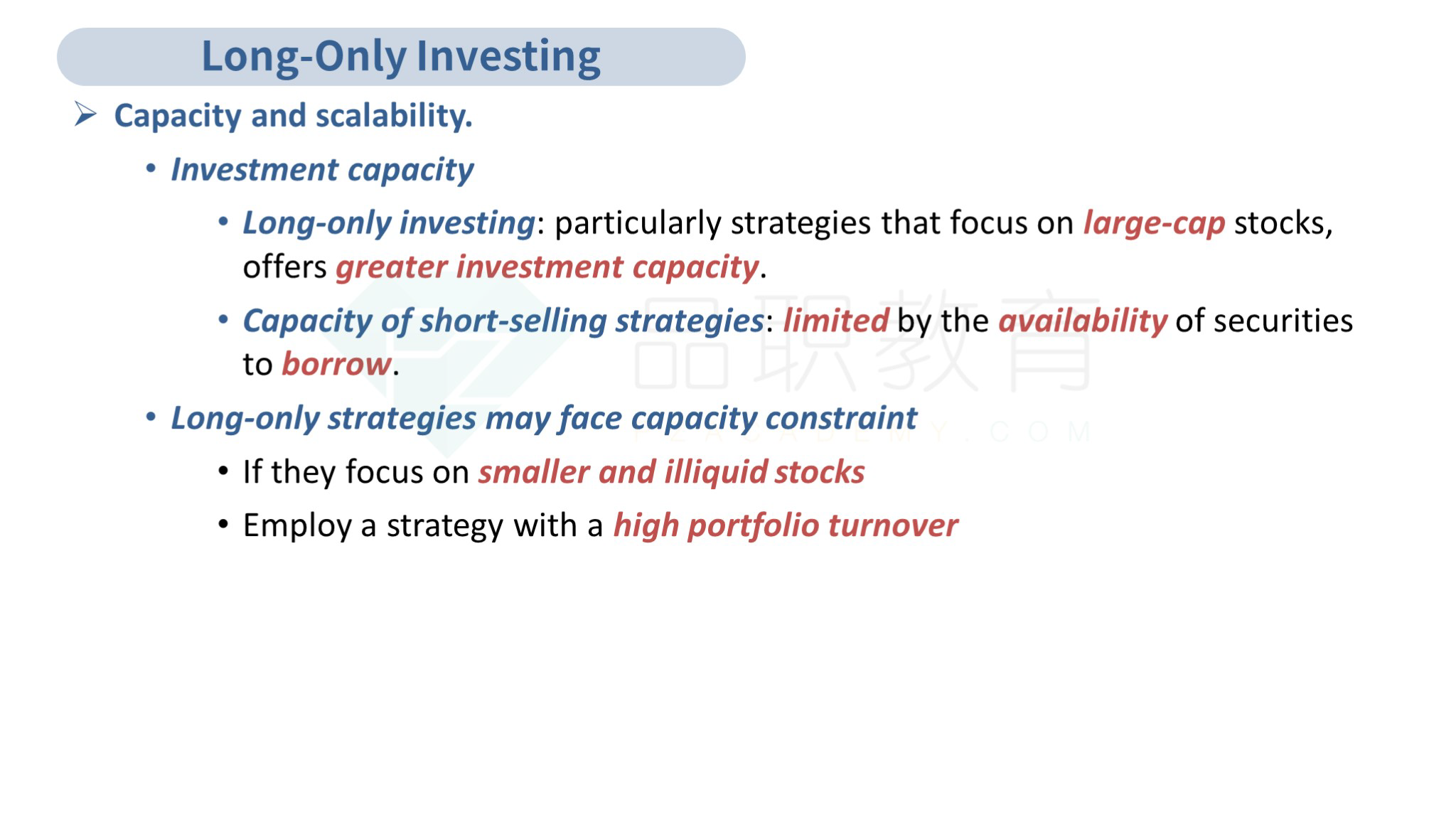

Statement 2 is correct because long-only investing generally offers greater investment capacity than other approaches, particularly when using strategies that focus on large-cap stocks. For large institutional investors such as pension plans, there are no effective capacity constraints in terms of the total market cap available for long-only investing.

请问 statement2知识点在讲义哪里?