NO.PZ2018062010000008

问题如下:

The followings are some descriptions of different kinds of duration. Which is most accurate?

选项:

A.

Macaulay duration is used for measuring the curve duration.

B.

Effective duration measures interest rate risk in terms of a nonparallel shift in the benchmark yield curve.

C.

A bond’s Macaulay duration always larger than its modified duration.

解释:

C is correct.

A bond’s Macaulay duration always larger than its modified duration. The relationship between Macaulay duration and modified duration is presented as following:

Where r is yield per period which is always larger than zero. Depending on this, the denominator ( 1 + r ) is always larger than 1. So a bond’s Macaulay duration always larger than its modified duration.

A is incorrect because Macaulay duration is used for measuring the yield duration, not the curve duration.

B is incorrect because effective duration measures interest rate risk in terms of a parallel shift in the benchmark yield curve.

考点:duration

解析:effective duration而非Macaulay duration衡量的是curve duration,A选项说法不正确。

有效久期衡量利率风险的时候,假设的是benchmark利率曲线发生一个平行移动,而不是nonparallel shift。parallel shift是指收益率曲线发生平行移动,也就是曲线上的每一个点都变动相同的幅度。B选项说法不正确。

修正久期等于麦考利久期/(1+一期的市场利率),市场利率通常情况下>0,因此(1+市场利率)通常情况下大于1。所以,C选项说法正确,当选。

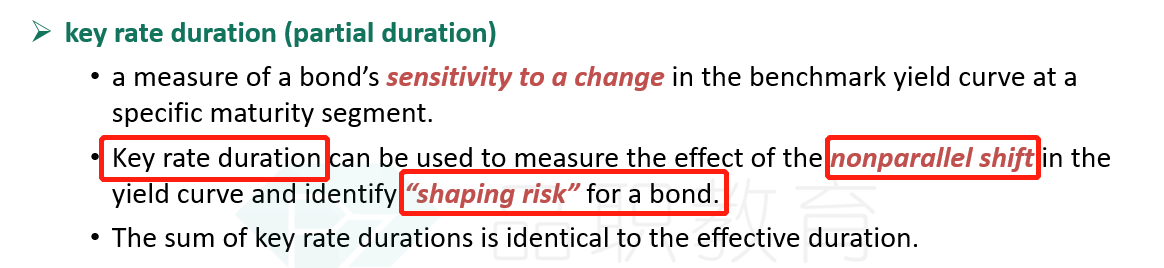

衡量nonparallel的是哪一种久期