NO.PZ201602060100001001

问题如下:

Percy Byron, CFA, is an equity analyst with a UK-based investment firm. One firm Byron follows is NinMount PLC, a UK-based company. On 31 December 2018, NinMount paid £320 million to purchase a 50 percent stake in Boswell Company. The excess of the purchase price over the fair value of Boswell’s net assets was attributable to previously unrecorded licenses. These licenses were estimated to have an economic life of six years. The fair value of Boswell’s assets and liabilities other than licenses was equal to their recorded book values. NinMount and Boswell both use the pound sterling as their reporting currency and prepare their financial statements in accordance with IFRS.

Byron is concerned whether the investment should affect his "buy" rating on NinMount common stock. He knows NinMount could choose one of several accounting methods to report the results of its investment, but NinMount has not announced which method it will use. Byron forecasts that both companies’ 2019 financial results (excluding any merger accounting adjustments) will be identical to those of 2018.

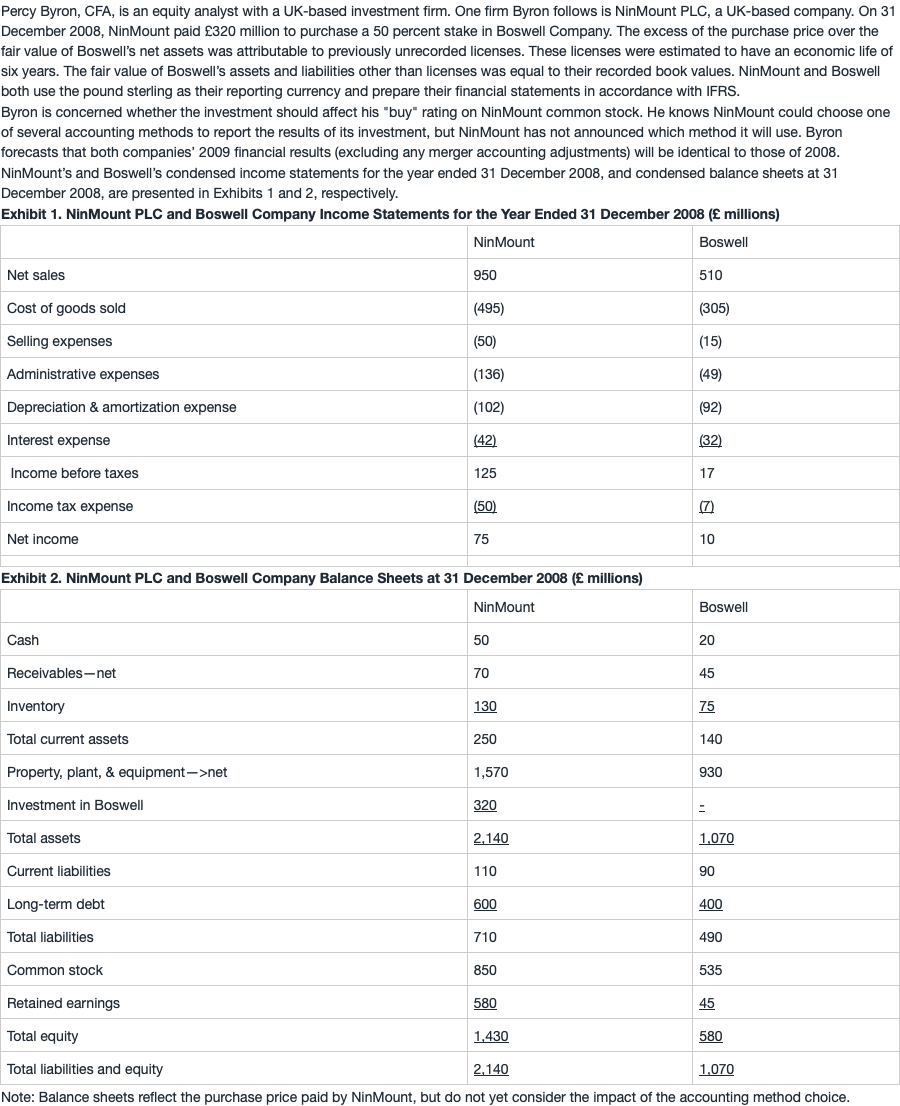

NinMount’s and Boswell’s condensed income statements for the year ended 31 December 2018, and condensed balance sheets at 31 December 2018, are presented in Exhibits 1 and 2, respectively.

Exhibit 1. NinMount PLC and Boswell Company Income Statements for the Year Ended 31 December 2018 (£ millions)

Exhibit 2. NinMount PLC and Boswell Company Balance Sheets at 31 December 2018 (£ millions)

Note: Balance sheets reflect the purchase price paid by NinMount, but do not yet consider the impact of the accounting method choice.

NinMount’s current ratio on 31 December 2018 most likely will be highest if the results of the acquisition are reported using:

选项:

A. the equity method.

B. consolidation with full goodwill.

C. consolidation with partial goodwill.

解释:

A is correct.

The current ratio using the equity method of accounting is Current assets/Current liabilities = £250/£110 = 2.27. Using consolidation (either full or partial goodwill), the current ratio = £390/£200 = 1.95. Therefore, the current ratio is highest using the equity method.

考点 : 不同合并会计报表方法对会计比率的影响 。

解析 :

current ratio =Current assets/Current liabilities

equity method不影响current asset和current liability, current ratio = £250/£110 = 2.27.

consolidation需要合并子公司的全部资产和负债 , current ratio=£390/£200 = 1.95

这道题没有goodwill,但要注意:不管有没有goodwill,partial goodwill与full goodwill的方式都不影响current asset的金额,因为goodwill属于长期资产。

因此,选项A正确。

※ 没有goodwill的原因:

题干中的信息: 超出net fair value的部分是由于要购买unrecorded licenses , 其他资产和负债的fair value=book value。这句话可以得到两个结论:

1. 子公司有一个未记账的资产,而在合并报表中,这项资产应该计入资产负债表。它的价值是并购对价超过子公司净资产fair value的部分。

相当于是NinMount公司花320买了Boswell公司一半的identifiable assets(包括已入账的也包括未入账的)。如果要买全部的identifiable assets则要花640:其中580是为了买已入账的identifiable assets,剩下的60根据题目信息,都是为了买这个unrecorded license。

2. 该项投资不产生goodwill,因为goodwill的定义是并购对价超过子公司net identifiable asset的部分,这个net identifiable asset既包含入账的资产,也包含之前没有记账但合并时应该记账的资产。因此本题并购的对价等于所购买的子公司的net identifiable asset,即没有goodwill。

Current asset 在equity method下不是应该减少吗?因为Cash减少了