NO.PZ2020011303000225

问题如下:

Suppose that the five-, ten-, and 30-year rates are 4%, 5%, and 6% with semiannual compounding. Calculate the duration and convexity of zero-coupon bonds with five-, ten-, and 30-years to maturity. What position in five- and 30-year bonds would have a duration equal to that of the ten-year bond? Compare the convexities of (a) the positions in the ten-year bond and (b) the position in the five- and 30-year bonds? Which of these positions will give the better return if (a) rates remain the same and (b) there are parallel shifts in the term structure?

选项:

解释:

The duration and convexities calculated by making one-basis-point changes are

We can construct a bond with a duration of 9.756 by investing β in the five-year

bond and 1−β in the 30-year bond where:

4.902β+29.126(1-β)=9.756

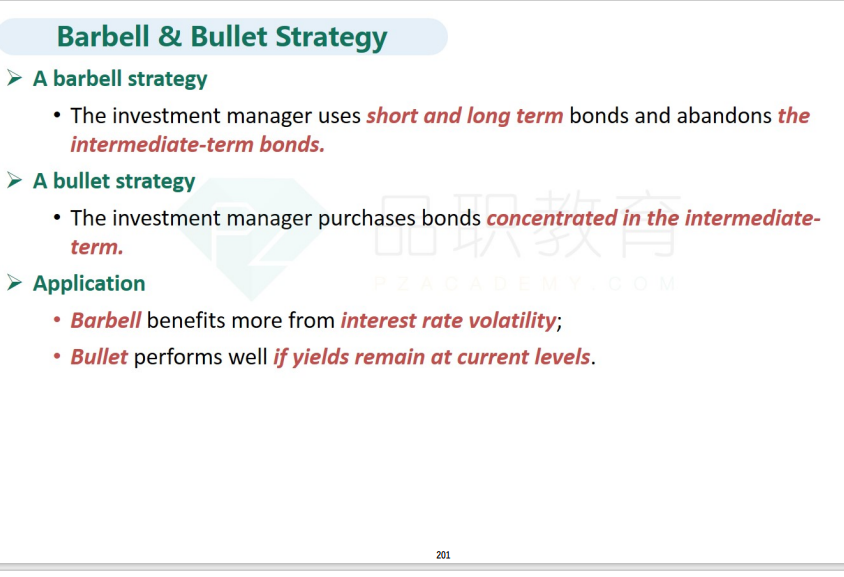

β is 0.7996, which we round to 0.8. We therefore invest 80% in the five-year bond and 20% in the 30-year bond. The ten-year bond investment (a bullet) has a convexity of 99.941 whereas the portfolio of five- and 30-year bonds (a barbell) has a convexity of about:

0.8×26.423+ 0.2×862.472 = 193.6

If rates remain the same the bullet will provide a yield of 5%, whereas the

barbell will provide a weighted average yield of 0.8 × 4 + 0.2 × 6 or 4.4%. The bullet will perform

better. When there are parallel shifts to the term structure, this effect is mitigated

somewhat by the barbell’s higher convexity, which leads to an immediate

improvement in the value of the barbell position. However, the bullet will

perform better for some non-parallel shifts.

The bullet will perform better. When there are parallel shifts to the term structure, this effect is mitigated somewhat by the barbell’s higher convexity, which leads to an immediate improvement in the value of the barbell position. However, the bullet will perform better for some non-parallel shifts.