NO.PZ2016062402000005

问题如下:

Given that x and y are random variables and a, b, c and d are constants, which one of the following definitions is wrong?

选项:

A.,

if x and y are correlated.

B.,

if x and y are correlated.

C.,

if x and y are correlated.

D.,

if x and y are uncorrelated.

解释:

Statement , as it is a linear operation. Statement C is correct, as in Equation:

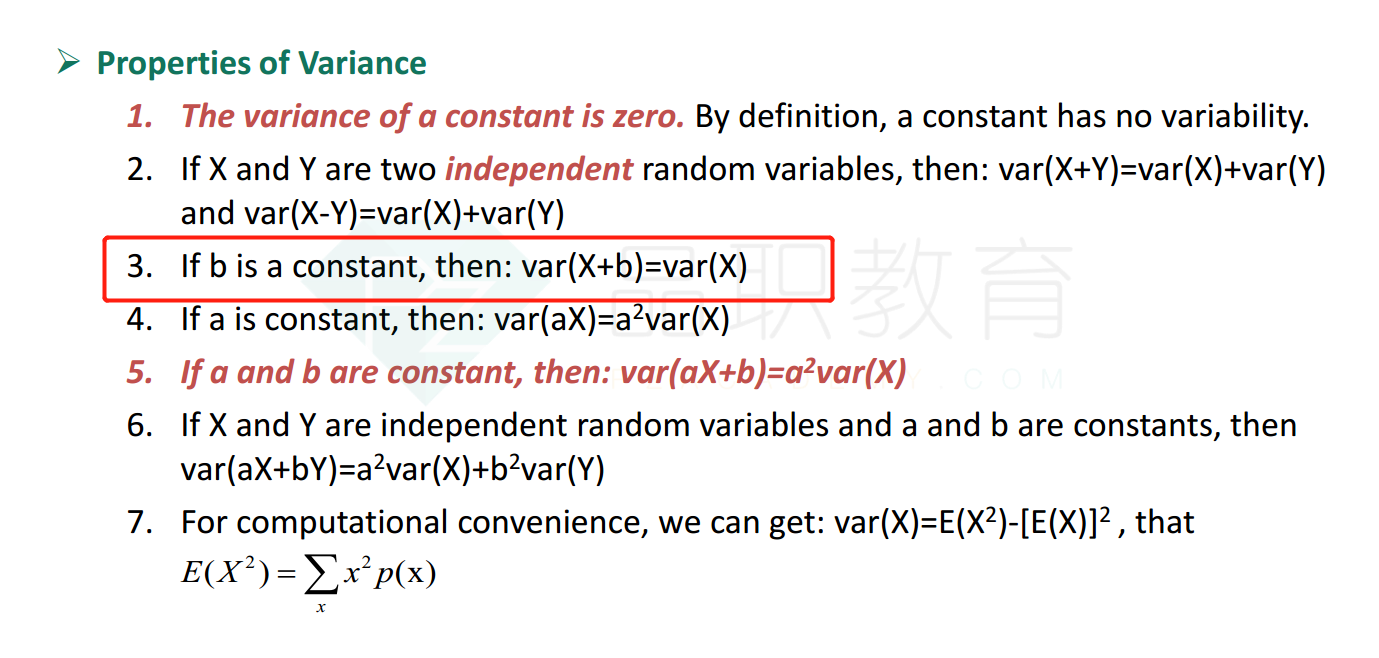

Statement D is correct, as the covariance term is zero if the variables are uncorrelated. Statement B is false, as adding a constant c to a variable cannot change the variance. The constant drops out because it is also in the expectation.

B项展开的公式是什么?这部分讲义讲的比较简单,何老师没有展开讲,做题时感觉都不会