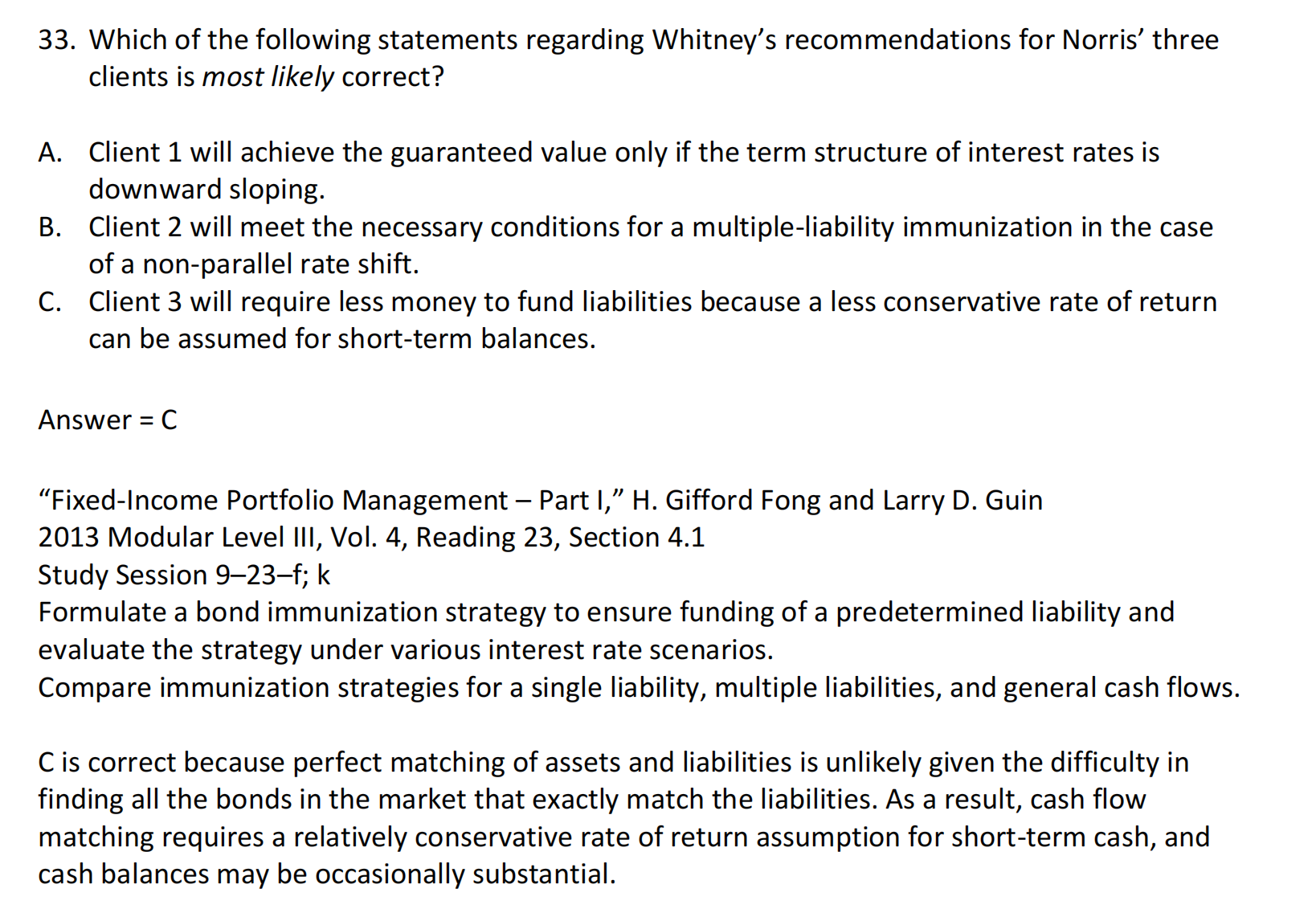

问题一:Mock题:Q33,(1)cash flow matching需要“更少的funding”?这个不是很理解。

(2)还有cash flow matching对于IRR的“假设更保守”?这个也不是很理解。

(1)“更少的funding”和(2)IRR的“假设更保守”,讲的地方有矛盾吗?

问题二:Mock题,statment 3为什么正确?

“spread duration 和interest rate risk无关”?

spread 的变化也会影响到bond pricing,对吗?

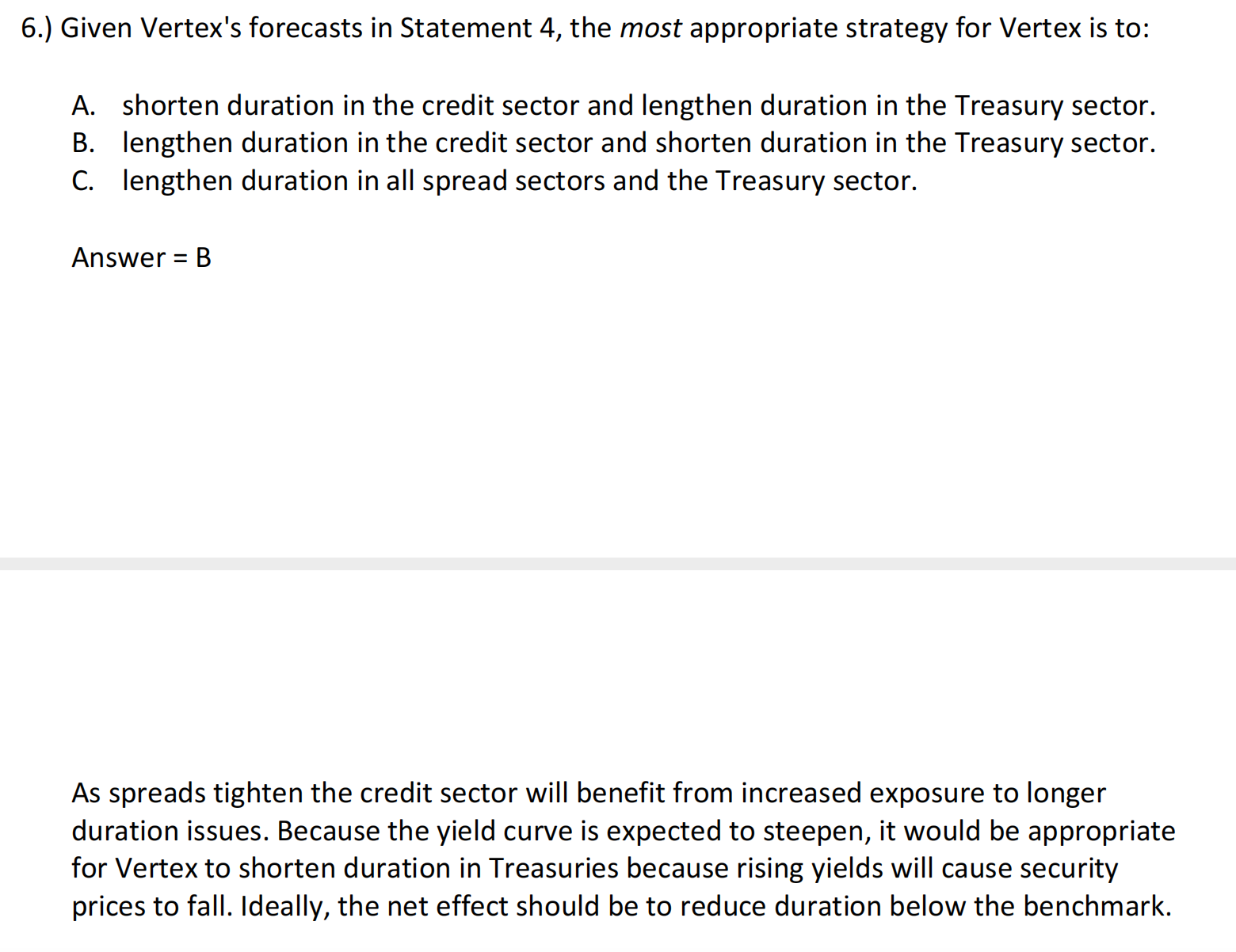

问题三:Mock题:Q6 “credit sector”和“Treasury sector”有什么不同?

long 哪一个,short 哪一个?

答案也不是很看得明白:“spreads tighten”怎么就后来“bond价格下降”呢?

“net effect”指的是什么和什么的作用相互抵消?

spread (下降25bpt)和yield(上升短期50 bpt和长期75 bpt) 的变化方向相反,此处哪一个比较主导?谢谢老师。

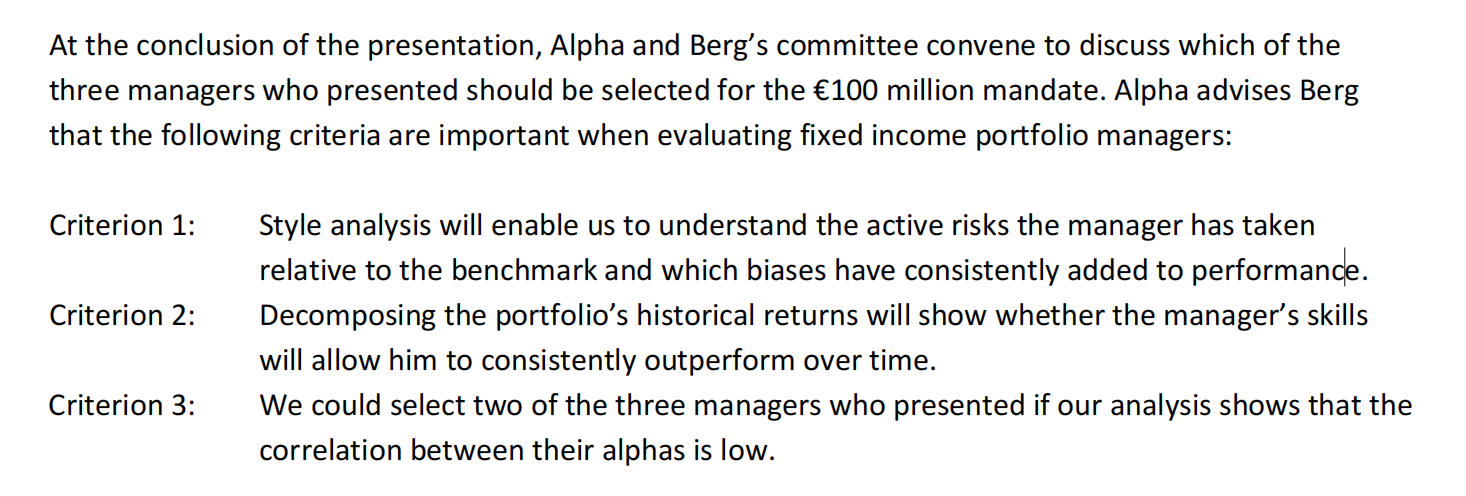

问题四:Mock题Q36,关于“Criterion 3正确”,不是很明白,为什么在选择基金经理的时候,需要找“alpha 相关性低”的?

是因为Diversification吗?

36. Which of the criteria outlined by Alpha is least accurate with respect to the selection of a fixed

income manager?

A. Criterion 1

B. Criterion 2

C. Criterion 3

Answer = B

B is correct because decomposing the portfolio’s historical returns is used to see if a manager has skill in security selection. Over long periods of time when fund fees and expenses are factored in, the realized alpha of fixed income managers has averaged very close to zero with little evidence of persistence.