NO.PZ2018070201000058

问题如下:

The point of tangency between the capital allocation line (CAL) and the efficient frontier of risky assets most likely identifies as the:

选项:

A.optimal riskly portfolio.

B.market portfolio.

C.global minimum-variance portfolio.

解释:

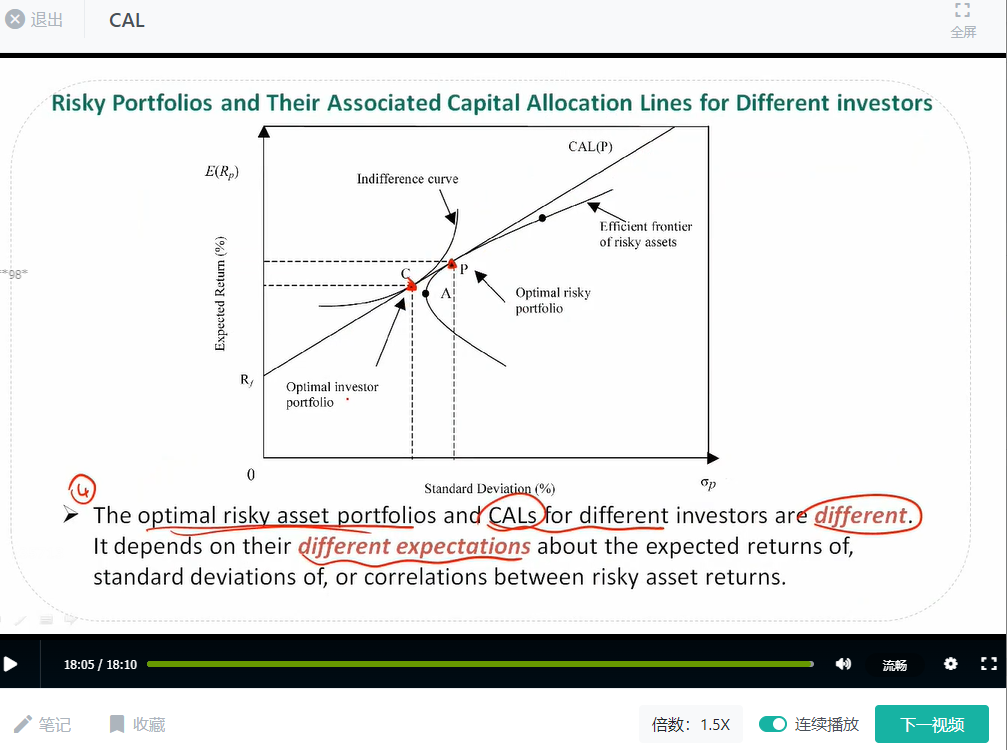

A is correct

The optimal risky portfolio is at the point of tangency between the capital allocation line and the efficient frontier of risky assets..

如题,按照我自己的理解,CAL是risk-free asset 与EF的切点连成的线,切点是risky asset portfolio,CML是risk-free asset 与EF的切点(切点是market portifolio)连成的线,是众多CAL中的最优解,只有这条线与Investor Utility有切点,但切点有没有定义,麻烦您解答一下,谢谢