NO.PZ2020011303000208

问题如下:

The term structure is initially flat at 5%, and an investor buys a five-year bond with a face value of USD 100 and a coupon of 4% at a spread of ten basis points. At the end of six months the term structure is flat at 6% and the spread is zero. Carry out a P&L decomposition.

选项:

解释:

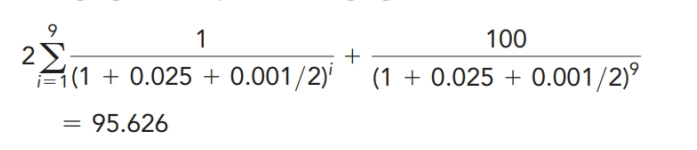

First we calculate the carry roll-down. The cash-carry is 2%. In this case, the assumption underlying the carry roll-down is that the term structure remains flat at 5%. (This is true for all three definitions of carry roll-down.) The initial price paid for the bond is

![]()

The price of the bond, if six months passes without rates changing or the spread changing, is

The carryroll-down is therefore: 2+95.626-95.199=2.427

This can also

be calculated as 0.0255 × 95.199.

The value of

the bond at the end of six months, assuming no spread change, is

After the

spread change is considered, the value of the bond is![]()

This leads to

the following table

The bond price in six months is 92.214 and the investor receives a coupon of 2.000 just before

92.214 + 2.000-95.199 = ﹣0.985

The P&L decomposition splits this into:

(a) A carry roll-down of 2.427,

(b) The impact of a term structure change of -3.782, and

(c) A spread change of 0.370.

﹣0.985 = 2.427-3.782 + 0.370

这10bps怎么理解?是coupon rate实际为4.1%?还是说折现时候利率加上10bps?